- What is a hammer letter and how does a hammer clause work?

- How is a hammer letter different from a Stowers demand or policy-limits demand?

- Will a hammer letter help my case or hurt it?

- What do Texas, California, and Illinois law say about insurers who refuse reasonable settlements?

- Texas: What is a Stowers letter and when does it trigger an insurer’s duty to settle?

- California: How do policy-limits demands create bad-faith exposure?

- Illinois: What is the duty to settle and how do policy-limits demands work?

- How do consent-to-settle clauses affect UM/UIM claims in TX, CA, and IL?

- When do insurers send hammer letters to their insureds and what happens next?

- What should plaintiffs include in a policy-limits demand to maximize effect?

- What negotiation timelines and follow-ups keep pressure on the insurer?

- What common insurer defenses could undercut a bad-faith claim?

- What evidence shows an offer was reasonable at the time?

- Do real-world crash statistics help explain why policy limits settle quickly?

- Should you ever contact the at-fault driver after a hammer letter goes out?

- Could hammer clauses create coverage conflicts or ethical issues for defense counsel?

- How can legal help make a difference in these insurance negotiations?

- Who is GoSuits and how can we help with a hammer letter or policy-limits demand?

- What reliable resources can you read to learn more?

What is a hammer letter and how does a hammer clause work?

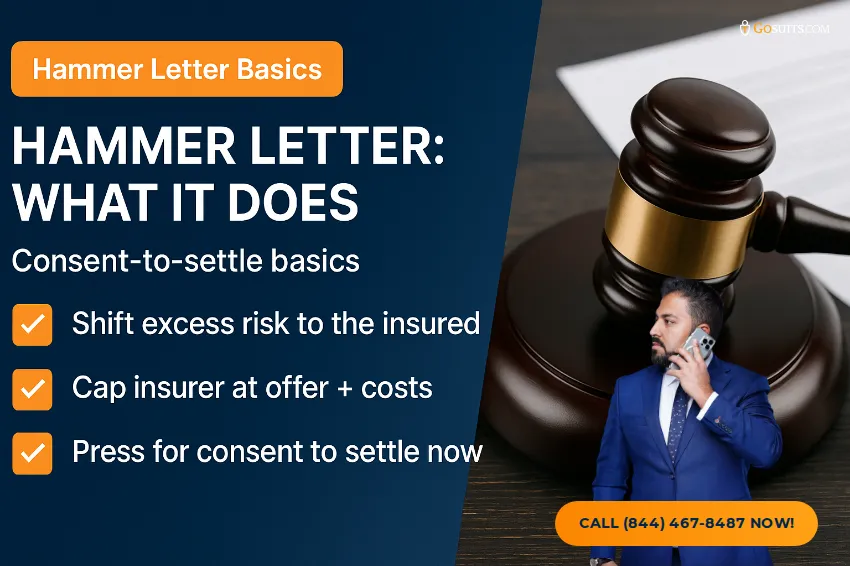

A hammer letter is a written notice from an insurance company to its policyholder telling them that the insurer recommends settling a claim for a specific amount, but the policyholder has a contractual “consent-to-settle” right. If the policyholder refuses consent, the insurer invokes the policy’s “hammer clause,” which limits the insurer’s future responsibility to the amount of the recommended settlement plus certain defense costs going forward. In plain terms, the letter says: if you do not agree to settle now, you may be personally responsible for any extra judgment and expenses beyond the settlement number we could have paid today.

These letters most often appear in professional liability policies and other policies with consent-to-settle language. The hammer clause is designed to discourage an insured defendant from rejecting a reasonable settlement because that rejection can expose both the insurer and the insured to bigger losses later. While the wording varies by policy and state, the overall function is similar: it shifts the risk of refusing a reasonable settlement back to the insured after the insurer has secured a settlement opportunity it believes is prudent.

By contrast, standard auto liability policies for everyday car accidents in places like Houston, Dallas, Austin, Los Angeles, San Diego, San Francisco, Chicago, and San Antonio often do not have consent-to-settle rights for the insured; in those common situations, the insurer decides whether to settle within policy limits and is governed by state “duty to settle” rules. That is where policy-limits demands, and in Texas the Stowers doctrine, come into play.

How is a hammer letter different from a Stowers demand or policy-limits demand?

It helps to separate two very different tools that show up in settlement negotiations:

- Hammer letter: Sent by an insurer to its own insured when a policy has a consent-to-settle clause. It warns that refusing to consent will cap the insurer’s responsibility at the proposed settlement amount and could shift the risk of any excess judgment to the insured.

- Policy-limits demand or Stowers demand: Sent by an injured claimant to the at-fault party’s liability insurer, offering to fully settle the claim within the policy limit by a clear deadline, backed by proof. If the insurer unreasonably refuses and an excess verdict follows, the insurer may be responsible for the full judgment for acting in bad faith or failing its duty to settle. In Texas, this doctrine is known as Stowers.

So a hammer letter is internal to the insured-insurer relationship when consent is required. A policy-limits or Stowers demand is external pressure from the injured person to the insurer to pay limits or face consequences.

Will a hammer letter help my case or hurt it?

A hammer letter can indirectly help if the defendant’s policy requires consent to settle and the insured has been reluctant. The letter pushes the insured toward accepting your settlement demand. Still, most consumer auto liability claims in Texas, California, and Illinois resolve without insured consent clauses, so your more direct lever is a well-crafted policy-limits demand, or in Texas, a proper Stowers letter.

What do Texas, California, and Illinois law say about insurers who refuse reasonable settlements?

While details vary, all three jurisdictions recognize that liability insurers can face consequences for unreasonably refusing to settle within policy limits when liability is reasonably clear and a prudent insurer would accept the offer.

- Texas recognizes the Stowers doctrine, rooted in the Texas Supreme Court’s line of cases beginning with G.A. Stowers Furniture Co. v. American Indemnity Co. Under Stowers and later decisions, a time-limited demand that meets certain requirements can create liability for the insurer if it declines and an excess verdict results.

- California recognizes a common-law duty to accept reasonable settlement demands within limits when liability is likely; failure can support bad-faith liability, including the amount of any excess judgment. California case law dating back to the 1950s has shaped these rules.

- Illinois recognizes a duty to settle when a reasonable offer is made and the probability of liability is high, and the insurer’s failure to accept may lead to liability for the excess judgment under bad-faith principles.

At a high level, Cornell Law School’s Legal Information Institute summarizes “bad faith” in the insurance context as an insurer’s breach of the implied covenant of good faith and fair dealing, which can include an unreasonable failure to settle within policy limits when appropriate. See Cornell LII: Bad faith.

Texas: What is a Stowers letter and when does it trigger an insurer’s duty to settle?

In Texas, a Stowers demand is a time-limited offer to the at-fault driver’s insurer to settle for policy limits that satisfy the criteria the Texas Supreme Court has laid out. If those elements are met and the insurer unreasonably refuses to settle, the insurer may be liable for the full amount of any subsequent judgment even if it exceeds policy limits.

What elements does a Texas Stowers demand typically require?

Texas Supreme Court decisions, including American Physicians Insurance Exchange v. Garcia and related cases, identify core components:

- Within policy limits: The offer is for an amount at or below applicable liability limits.

- Full release: It offers a full, unconditional release of the insured for the claims at issue if accepted.

- Reasonable terms: The terms would be accepted by an ordinarily prudent insurer considering the likelihood and magnitude of an adverse verdict.

- Clear liability and damages support: The demand is backed by evidence that fairly informs the insurer of liability exposure and damages.

- Deadline: A reasonable time limit to accept, stated clearly and in writing.

- Coverage alignment: The demand seeks to settle claims that are actually covered by the policy.

Texas courts also address multi-claimant situations where policy limits are inadequate. The Texas Supreme Court has permitted insurers to settle reasonably with one claimant even if other claimants remain, provided the settlements are reasonable under the circumstances. The details become fact-intensive and demand careful analysis before sending or responding to a Stowers demand.

How does UM/UIM intersect with consent-to-settle in Texas?

Texas UM/UIM coverage is created by statute. The Texas Insurance Code addresses uninsured and underinsured motorist coverage requirements. See Texas Insurance Code Chapter 1952. Settlement-without-consent clauses in UM/UIM policies have been litigated in Texas. Texas case law holds that such clauses cannot be used to avoid coverage absent prejudice to the insurer’s subrogation rights, which turns on specific facts and timing relative to settlements with the at-fault driver. Whether and when a consent-to-settle clause applies can affect how you structure a demand and communicate with the UM/UIM carrier.

Where in Texas should you consider sending a Stowers demand?

Every claim is unique, but Stowers demands appear frequently in high-impact collisions across Texas, including Houston, Dallas, Austin, and San Antonio. Serious-injury cases with limited liability policies often prompt timely demands when liability is clear and damages exceed limits.

How do policy-limits demands create bad-faith exposure in California?

California recognizes a common-law duty to accept a reasonable settlement demand within policy limits when liability is reasonably clear and the potential judgment may exceed limits. Seminal California Supreme Court decisions, including Comunale v. Traders & General Ins. Co., 50 Cal. 2d 654, and Crisci v. Security Ins. Co., 66 Cal. 2d 425, explain that an insurer that unreasonably refuses such a demand can be liable for the entire excess judgment and other foreseeable damages.

What should a California limits demand look like?

- Clear offer and deadline: A written, time-limited demand within limits.

- Complete release: A release of the insured and appropriate parties for covered claims.

- Liability and damages documentation: Police reports, photographs, medical records and bills, loss-of-income documentation, and other proof supporting a likely verdict above limits.

- Payment logistics: Payee details, W-9 if requested, and handling of liens.

- Reasonable conditions only: Avoid unnecessary conditions that could be used as a pretext to claim the offer was not “reasonable.”

California does not require a specific form. The question is whether the offer is reasonable and whether a prudent insurer would have accepted it under the circumstances when made.

How do California UM/UIM consent-to-settle rules work?

California’s UM/UIM statute expressly addresses consent-to-settle and subrogation. Under California Insurance Code section 11580.2, the policy may include requirements designed to protect the insurer’s reimbursement rights. See Cal. Ins. Code § 11580.2. A claimant who intends to settle with the at-fault driver should consider the UM/UIM carrier’s consent and notice requirements to avoid jeopardizing UM/UIM benefits. The statute and case law include mechanisms for the UM/UIM insurer to protect subrogation rights, including advancing settlement funds to preserve those rights in some scenarios.

Where in California do policy-limits demands commonly arise?

In urban corridors such as Los Angeles, San Diego, and San Francisco, high medical costs and lost wages can rapidly exceed typical bodily injury limits. A clear, time-limited demand can spotlight the insurer’s risk and prompt a timely settlement.

Illinois: What is the duty to settle and how do policy-limits demands work?

Illinois recognizes a common-law duty to settle when a reasonably prudent insurer would accept a within-limits demand given likely liability and potential exposure. The Illinois Supreme Court in Haddick ex rel. Griffith v. Valor Insurance, 198 Ill. 2d 409, articulated that an insurer may be liable for the amount of an excess judgment where it fails to give equal consideration to the insured’s interest in avoiding personal liability.

What should a policy-limits demand in Illinois include?

- Time-limited, within-limits offer that fully releases the insured for covered claims.

- Comprehensive documentation supporting liability and damages likely in excess of limits.

- Clear settlement mechanics, including payee information and lien handling.

- Notice to UM/UIM carrier if applicable to address subrogation concerns.

How do Illinois UM/UIM consent-to-settle rules work?

Illinois statute sets rules for UM/UIM coverage, including how settlements with the tortfeasor interact with the UM/UIM carrier’s subrogation rights. See 215 ILCS 5/143a-2. Under the statute, procedures exist for notifying the UM/UIM insurer and for the insurer to advance funds to preserve subrogation rights in certain circumstances. Failing to follow these procedures can complicate or reduce UM/UIM recovery.

Where in Illinois do these issues most often surface?

In metropolitan Chicago and surrounding counties, medical care costs and lost income commonly outstrip lower policy limits. Carefully timed, well-supported policy-limits demands can accelerate resolution.

How do consent-to-settle clauses affect UM/UIM claims in TX, CA, and IL?

UM/UIM coverage is heavily statute-driven and differs by state:

- Texas: Chapter 1952 of the Insurance Code governs UM/UIM. See Tex. Ins. Code ch. 1952. Texas courts have limited the effect of settlement-without-consent clauses unless the UM/UIM insurer can show prejudice to its subrogation rights. This means notice and timing matter when working with both the at-fault driver’s insurer and your own UM/UIM carrier.

- California: The UM/UIM statute authorizes contract provisions that protect subrogation. See Cal. Ins. Code § 11580.2. If you plan to accept the liability carrier’s limits, you should coordinate with your UM/UIM insurer so your UM/UIM claim remains intact.

- Illinois: The Illinois Insurance Code section addressing UM/UIM sets notice and advancement mechanisms that affect consent-to-settle dynamics. See 215 ILCS 5/143a-2.

The overlap between policy-limits demands and UM/UIM varies by state. In all three, preserving UM/UIM rights typically requires coordinated timing and written notice steps before you sign a release with the at-fault driver.

When do insurers send hammer letters to their insureds and what happens next?

Insurers send hammer letters when a policy contains a consent-to-settle clause and the insurer believes it has obtained a reasonable, within-limits settlement opportunity that the insured may reject. You commonly see this in certain professional liability and errors-and-omissions policies. The letter usually:

- Identifies the proposed settlement amount and terms.

- Explains the insurer’s evaluation and risks of an excess verdict.

- Invokes the hammer clause, warning that refusing consent will cap the insurer’s future responsibility at the proposed settlement figure plus defined defense costs after the refusal.

- Sets a short deadline to consent.

If the insured consents, the claim typically resolves. If the insured refuses, the insurer may continue to defend under a reservation of rights and will document that any later excess is the insured’s problem under the hammer clause. Defense counsel’s ethical duties become complex when the insured’s interest in avoiding excess liability diverges from the insurer’s cost-control goals.

What should plaintiffs include in a policy-limits demand to maximize effect?

For injured plaintiffs in Texas, California, and Illinois, a concise, complete policy-limits demand can move an insurer off the fence:

- Clear settlement amount: Demand the full available per-person or per-occurrence bodily injury limit, or a specific amount within limits.

- Unconditional release: Offer a full release of the insured and appropriate entities upon timely payment.

- Liability proof: Police report, crash diagram, photos, witness statements, and admissions.

- Damages proof: Medical records and bills, diagnostic imaging reports, therapy notes, wage loss documentation, and statements explaining pain, functional limits, and future care needs where supported by records.

- Deadline: A reasonable period that considers the case complexity and record volume. Time-limited demands often run 15 to 30 days for straightforward cases, and longer for complex losses.

- Payment details: Who to pay, tax form if needed, lien information, and method of delivery.

- Coverage clarity: Identify the claim types you will release to avoid coverage-based objections.

A well-built demand in cities like Houston, Dallas, Austin, Los Angeles, San Diego, San Francisco, and Chicago gives the claims adjuster a complete file and reduces room for later arguments that the offer was unclear or impossible to accept.

What negotiation timelines and follow-ups keep pressure on the insurer?

- Set a reasonable clock: Choose a deadline that matches case complexity and the amount of documentation provided.

- Confirm receipt: Use certified mail or electronic delivery with confirmation.

- Offer access: Invite the insurer to request any additional reasonable documents within the deadline, in writing.

- Follow up once: A polite reminder a few business days before the deadline can avoid “we never saw it” disputes.

- Document all communications: Keep a timeline of offers, requests, and responses to evaluate reasonableness later.

What common insurer defenses could undercut a bad-faith claim?

Insurers often argue:

- Ambiguous or conditional offer: The demand had unclear terms, impossible conditions, or did not offer a full release.

- Insufficient time: The deadline was unreasonably short given the case complexity.

- Coverage dispute: The claim involved uncovered losses or excluded conduct.

- Liability uncertainty: Key facts were still in dispute so a prudent insurer would not have paid limits at that time.

- Missing documentation: The demand did not include essential records to evaluate damages or causation.

- Multiple claimants: Limits had to be apportioned among multiple injured persons in good faith.

Anticipating these defenses when drafting your demand makes it stronger and clearer.

What evidence shows an offer was reasonable at the time?

Reasonableness is judged at the time the offer was made, not in hindsight. Helpful items include:

- Police crash reports and citations showing fault.

- Event data recorder or video confirming speed, impact, or signals.

- Medical records and bills reflecting diagnoses, treatment, and cost.

- Wage documentation showing work limitations or job loss.

- Comparable verdicts or settlements in the venue demonstrating likely exposure beyond limits.

- Insurer’s internal notes or correspondence if they acknowledge high exposure before refusal.

Do real-world crash statistics help explain why policy limits settle quickly?

They do. Serious crashes create significant losses that can exceed standard liability limits quickly, especially in large metro areas like Houston and Los Angeles. National safety data show the scope of severe crashes:

- Crash fatality burden: The Centers for Disease Control and Prevention reports that motor vehicle crashes are a leading cause of injury and death in the United States and impose substantial economic costs from medical care and lost productivity. See CDC Motor Vehicle Safety.

- Annual deaths: NHTSA’s Fatality Analysis Reporting System shows tens of thousands of roadway deaths annually. See NHTSA’s 2022 national traffic crash data overview, which details fatalities and risk patterns across the country. NHTSA 2022 Traffic Fatalities.

When injuries are severe, medical bills and lost income alone may surpass common policy limits, which is why time-limited policy-limits demands are common in high-damages cases.

Should you ever contact the at-fault driver after a hammer letter goes out?

Generally, no. Direct contact with a represented party can create complications and ethical issues. Communication about settlement should flow through the insurer or defense counsel. If defense counsel indicates that the insured’s consent is required under a consent-to-settle clause, provide the complete documentation to the insurer and counsel so they can evaluate the offer. In Texas Stowers contexts, the focus is the insurer’s decision, not the insured’s consent.

Could hammer clauses create coverage conflicts or ethical issues for defense counsel?

They can. When a hammer letter shifts the risk of an excess verdict onto the insured, the insured may want to settle, while the insurer may want to continue litigating if it believes the case can be defended within the hammer cap. Defense counsel retained by the insurer must still protect the insured’s interests and communicate the risks posed by the hammer clause and any excess exposure. In some circumstances, the insured may seek separate personal counsel to advise on settlement and exposure.

How can legal help make a difference in these insurance negotiations?

Insurance settlement law is technical and state-specific. The difference between a routine demand and a Stowers-compliant or policy-limits demand can decide whether an insurer pays limits promptly or digs in. The timing, documentation, wording, and handling of UM/UIM consent and lien issues all matter. Coordinated strategy is especially important in Texas, California, and Illinois, where the rules are similar in spirit but different in implementation.

Who is GoSuits and how can we help with a hammer letter or policy-limits demand?

If your injury claim involves policy limits, a potential Stowers demand, a hammer clause, or UM/UIM consent-to-settle issues in Texas, California, or Illinois, our team is ready to step in promptly and work the problem from every angle.

- What availability and communication do we offer?

We are available 24/7 with immediate free consultations by phone or secure video at any time. We keep you updated with clear timelines, copies of critical letters, and plain-language status messages. We provide multilingual customer service, with Spanish and Farsi support available around the clock. When a time-limited demand is running, we set specific communication checkpoints so you are never left guessing. - What are our fee policies and cost transparency?

We offer a contingency arrangement described here: No win, No Attorney Fees. We do not add hidden administrative fees. From the outset, you receive a written explanation of potential case costs, how liens are handled, and how a policy-limits settlement is disbursed. If a lawsuit becomes necessary, we discuss projected expenses and options before any step is taken. - How do our tools and case workflow help your claim?

We built an internal personal-injury software platform that helps us gather records faster, track insurer obligations and deadlines, and assemble complete, time-limited demands with the right proof. It also supports lawsuit drafting, e-filing, and discovery scheduling so litigation moves without delay when needed. We are a law firm that invests in forward-looking systems to compete with insurance carriers on speed, organization, and precision. - What is our experience and track record?

Our attorneys have 30 years of combined experience and have litigated more than 1,000 cases. Settlement and verdict results are posted here: Prior Cases. In complex matters such as product liability, 18-wheeler collisions, brain injuries, spinal injuries, and other serious cases, we retain qualified in-state professionals to provide testimony on liability and damages where appropriate.

We handle severe injury and complex litigation across Texas, California, and Illinois.

Awards and recognitions include:

- #1 settlements and verdicts across multiple U.S. counties according to TopVerdict.

- Top 100 Settlement in Texas.

- Sean Chalaki named Top 40 Under 40 by National Trial Lawyers.

- Recognized by Best Lawyers for 2023, 2024, and 2025.

- Selected to Super Lawyers since 2021.

- How are we involved in the community?

We participate in local schools, chambers of commerce, and non-profit foundations. Team members serve on boards of trial lawyer organizations including the Texas Trial Lawyers Association and are active in consumer rights protection groups. Community engagement keeps us connected to the real-world challenges clients face after serious crashes. - What services do we provide in hammer letter and policy-limits matters?

We evaluate coverage and applicable limits, build comprehensive time-limited demands, and manage communications with the insurer to reduce ambiguity. In Texas, we prepare Stowers-compliant demands tailored to the facts and venue. In California and Illinois, we structure policy-limits demands with the documentation and timing most likely to prompt acceptance. When UM/UIM is in play, we coordinate consent-to-settle steps and subrogation protections to keep your benefits intact. If the insurer refuses to act reasonably, we are prepared to file suit and pursue recovery through verdict and post-trial motions. - Where are we located and how do we help immediately?

We serve clients across Texas, California, and Illinois, with attorneys and staff available 24/7 at our offices to begin intake, secure evidence, and send preservation notices. We can dispatch investigators to crash locations in major metros including Houston, Dallas, Austin, San Antonio, Los Angeles, San Diego, San Francisco, and Chicago. We move quickly to gather medical records and wage documentation, set up claims, and prepare policy-limits or Stowers demands supported by the evidence carriers need to pay promptly. - What sets our approach apart?

We are not a volume firm. We focus on careful case development, thorough documentation, and clear demand packages that anticipate insurer objections. Our internal systems track every deadline and item requested, which helps keep leverage where it belongs. You will always know the next step and the reason behind it.

A free consultation can clarify whether a hammer clause, Stowers demand, or UM/UIM consent issue is likely in your situation, what records we would gather first, and how we would time a policy-limits demand to make acceptance as straightforward as possible for the insurer.

Reliable resources

- Cornell Law School Legal Information Institute: Bad faith — Overview of insurance bad faith principles and the implied covenant of good faith and fair dealing.

- Texas Insurance Code Chapter 1952 — Statutory framework for UM/UIM coverage in Texas.

- California Insurance Code § 11580.2 — California UM/UIM statute including provisions touching consent-to-settle and subrogation.

- Illinois Insurance Code 215 ILCS 5/143a-2 — Illinois UM/UIM provisions with notice and advancement mechanisms.

- CDC Motor Vehicle Safety — National data and research on motor vehicle injuries and deaths.

- NHTSA: 2022 Traffic Fatalities — National fatality statistics and trends from the Fatality Analysis Reporting System.

Case law regarding Texas Stowers doctrine and California and Illinois duty-to-settle rules is widely available through Google Scholar and CourtListener. Look for Texas Supreme Court decisions discussing Stowers demands and California Supreme Court decisions such as Comunale and Crisci, as well as Illinois Supreme Court decisions including Haddick.