- What Are California’s Rideshare Insurance Periods and Why Do They Matter?

- When Does Uber and Lyft’s $1 Million Coverage Actually Apply?

- What Happens When the App Is On but No Ride Has Been Accepted?

- What If the Driver Was Off the App Entirely?

- Who Can Make a Claim Under the $1 Million Policy?

- How Does Uninsured and Underinsured Motorist Coverage Work in California Rideshare Cases?

- What Evidence Do You Need to Prove Which Coverage Applies?

- What Are the Deadlines for Filing a Rideshare Injury Claim in California?

- How Does California’s Comparative Fault Rule Affect a Rideshare Claim?

- How Gosuits Irvine Helps Rideshare Injury Victims in California

- References / Resources

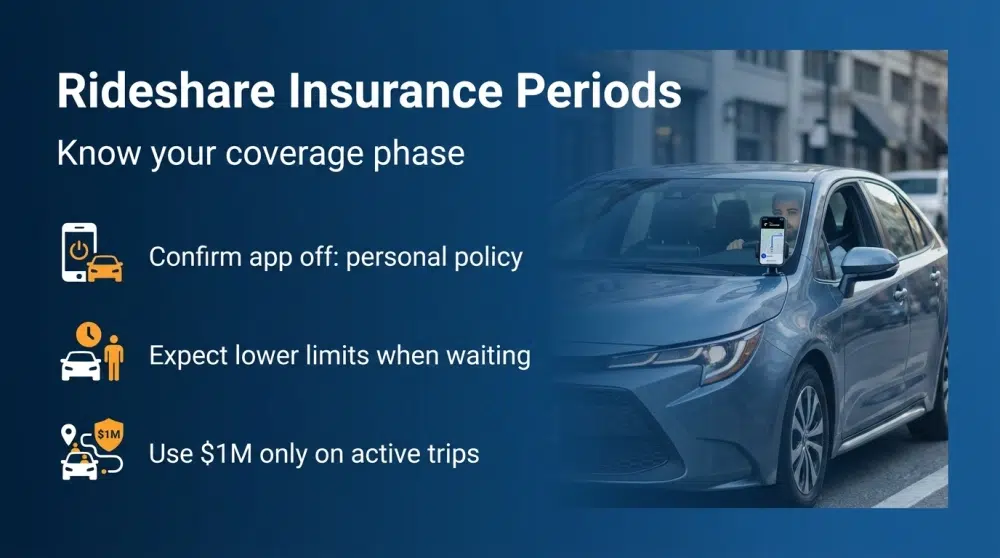

What Are California’s Rideshare Insurance Periods and Why Do They Matter?

If you have been injured in an Uber or Lyft accident anywhere in California whether on the I-405 through the Irvine Spectrum, on the 101 in downtown Los Angeles, or on surface streets in Santa Ana, one question will shape everything about your injury claim: what was the driver doing on the app at the exact moment of the crash?

So California treats rideshare driving as a series of phases for insurance purposes, and the phase that was active at the moment of impact is what determines your coverage. That’s not some technicality. The spread runs from about $50,000 all the way up to $1 million, depending on what the driver was doing on the app. Big difference. Whether you’re a passenger, another driver on the road, a pedestrian, or even a rideshare driver who got hit by somebody else, knowing which period you’re dealing with is kind of where everything starts.

If you want the actual legal source, it’s California Public Utilities Code §5433. [1] That statute covers Transportation Network Companies – TNCs for short and sets the minimum insurance for each phase of driver activity. Oversight falls to the California Public Utilities Commission. [2] Pretty broad reach, too. The rules apply to Uber and Lyft both, and to every participating driver in California, from Irvine down through Los Angeles and over to Pasadena.

When Does Uber and Lyft’s $1 Million Coverage Actually Apply?

The $1 million figure you may have seen in headlines or rideshare company marketing refers to the liability coverage that takes effect during what California law calls the active trip phase. Under California Public Utilities Code §5433(b), once a driver has accepted a ride request through the Uber or Lyft platform, and from that moment until the transaction is complete and the passenger has exited, the following minimums apply: [1]

- $1,000,000 in primary liability coverage for death, personal injury, and property damage.

- Uninsured motorist (UM) and underinsured motorist (UIM) coverage of at least $60,000 per person and $300,000 per incident, which is primary over any other applicable UM/UIM coverage and is solely the TNC’s obligation.

- The insurer providing this coverage has the duty to defend and indemnify the insured.

This active-trip coverage is primary it does not require the driver’s personal auto policy to deny the claim first. [1] That distinction matters because it removes one of the most common excuses insurers use to delay paying injured people.

In practical terms, this period covers the following scenarios: you are a passenger riding from Newport Beach to John Wayne Airport; a pedestrian is struck by an Uber driver who just accepted a trip on the SR-73 Toll Road; or a driver on the 405 is hit by a Lyft driver who already has a passenger in the car. In all of those situations, the $1 million policy is potentially available.

Personal injury lawyers who handle rideshare cases pay close attention to the precise timestamp of the ride acceptance versus the crash, because that single data point can unlock dramatically different coverage. Our knowledge base article on what to do after an Uber or Lyft accident walks through exactly what to document at the scene to preserve this critical information.

What Happens When the App Is On but No Ride Has Been Accepted?

A large number of rideshare crashes occur during the second phase: the driver is logged into the Uber or Lyft app and available to accept rides, but has not yet matched with a passenger. This is sometimes called the “waiting period” or Period 1 in insurance terminology.

Under California Public Utilities Code §5433(c), during this phase a different and lower set of minimums applies: [1]

- At least $50,000 per person for death and personal injury.

- At least $100,000 per incident for death and personal injury.

- At least $30,000 for property damage.

- An additional excess coverage layer of at least $200,000 per occurrence that the TNC must also maintain to cover liability arising from this period that exceeds the base limits.

- The insurer providing coverage under this subdivision is the only insurer with the duty to defend any liability claim arising from an accident in this period.

These limits are meaningful but far lower than the $1 million active-trip policy. If you are rear-ended on the I-5 near Costa Mesa by a rideshare driver who was online but waiting for a ride request, you are likely dealing with the Period 1 limits, not the $1 million policy. Serious injuries with significant medical bills can easily exceed $50,000 per person, which is why understanding the coverage period is so critical to evaluating your options.

California law also provides that if the driver’s personal auto insurance lapses or ceases to exist during this period, the TNC must provide the coverage beginning with the first dollar of any claim. [1] The rideshare company cannot simply walk away because its driver let their personal policy lapse.

What If the Driver Was Off the App Entirely?

When a driver is not logged into the Uber or Lyft platform at all whether they are driving for personal reasons or simply between shifts, neither Uber’s nor Lyft’s TNC policy applies. The crash is governed by the driver’s personal auto insurance only, subject to whatever limits and exclusions that policy contains.

Here’s where it can get ugly. The driver’s personal policy might have low limits, or there could be a coverage gap you weren’t expecting, and either way the injured person ends up squeezed. California does require minimum liability coverage under the Insurance Code, [3] but those minimums are kind of laughable for anything past a fender-bender. So you might need to lean on your own uninsured or underinsured motorist coverage, assuming you have it. Or start digging into whether someone else on the road shares the blame.

One thing that keeps popping up in these cases : was the app really off? Uber and Lyft keep timestamped trip logs, every login, every ride accepted, every trip wrapped. Attorneys grab those records in discovery. It’s pretty routine. And if there’s any doubt about what the driver was doing at the moment of impact, the data tends to clear it up fast. Sometimes it even flips the whole coverage analysis if the company got the period wrong the first time around.

Who Can Make a Claim Under the $1 Million Policy?

The $1 million active-trip coverage is not limited to passengers. Several categories of injured people may be able to access this coverage depending on the circumstances:

- Passengers in the Uber or Lyft vehicle who are injured through the driver’s fault or through the fault of a third party.

- Occupants of other vehicles struck by an Uber or Lyft driver who was in active-trip status.

- Pedestrians and cyclists injured by an Uber or Lyft driver during an active trip.

- The rideshare driver themselves, if injured by a third party while transporting a passenger, UM/UIM coverage is specifically required during this period.

From the defendant’s perspective, if you are an Uber or Lyft driver accused of causing an accident during an active trip, the company’s $1 million policy should provide a defense subject to the policy terms and the specific circumstances of the claim. Both plaintiff and defense interests in these cases require careful analysis of which coverage tier applies and what the policy actually covers.

For passengers injured while riding on the I-5 between Irvine and Los Angeles, or on the 405 through the Westside, the active-trip $1 million policy is a critical safety net. However, accessing it is not automatic, claims must be properly presented, and insurers will scrutinize the trip data, police reports, and medical records before agreeing on liability and damages.

How Does Uninsured and Underinsured Motorist Coverage Work in California Rideshare Cases?

California Insurance Code requires UM/UIM coverage in certain circumstances, and California Public Utilities Code §5433(b)(2) specifically mandates that during an active trip, Uber and Lyft must provide UM/UIM coverage of at least $60,000 per person and $300,000 per incident. [1] This coverage is primary over any other applicable UM/UIM policy and is the TNC’s sole obligation. [4]

What does this mean for injured parties? If a Lyft passenger is injured because a third-party driver ran a red light in Fullerton and that at-fault driver carries only the state minimum liability coverage the passenger can look to Lyft’s UIM coverage for additional compensation if the third party’s policy is insufficient. This is a significant protection that did not exist uniformly before California enacted its TNC insurance statutes.

The interaction between personal UM/UIM policies, the TNC’s required UM/UIM coverage, and any health insurance liens requires careful coordination. California has specific rules on policy stacking and on which insurer pays first that affect the net recovery an injured person actually receives. [5] Navigating these layers without guidance from someone familiar with California rideshare insurance law frequently leads to people accepting settlements far below their actual damages.

If you or someone you care about has been injured in a rideshare accident in Irvine, Los Angeles, or anywhere in Southern California, speaking with personal injury lawyers before any insurer conversation can help you understand which coverages apply and in what order.

What Evidence Do You Need to Prove Which Coverage Applies?

The single most contested issue in most rideshare injury cases is the coverage period: which phase was the driver in? Proving this requires specific evidence, much of it in digital form that can disappear quickly.

Trip and App Records

Uber and Lyft maintain internal logs showing when drivers log in, when they accept or decline requests, when trips begin and end, and when drivers log off. These records can be obtained through litigation discovery or, in some cases, by requesting them directly from the company before litigation begins. Screenshots of the app at the time of the crash, if taken by a witness, can be helpful but authenticated data from the company itself carries more evidentiary weight.

Police and CHP Collision Reports

In Southern California, crashes on state highways are typically handled by the California Highway Patrol. If the accident occurred on the I-5 near Irvine or on the 405 near Los Angeles, you can request the collision report through the CHP. [6] For crashes on city streets in areas like Santa Ana or Anaheim, the local police department maintains the records. The collision report will not always identify the rideshare status, but it provides the foundational facts about time, location, and parties involved.

Medical Documentation

Your medical records from the emergency department, follow-up care, and any specialist treatment document the injuries and their connection to the crash. In the Irvine and Los Angeles areas, trauma centers affiliated with major hospital systems maintain these records. Request them promptly, delays in obtaining records can complicate later claims.

Witness Statements and Video

Traffic cameras, business surveillance systems, and dashcam footage can capture the crash and its circumstances. Retention periods for this footage vary; requests must be made quickly. In busy commercial areas like the Irvine Spectrum or downtown Los Angeles, there is often more footage available than people expect.

DMV SR-1 Filing

California law requires drivers involved in accidents causing injury, death, or property damage above the statutory threshold to file a Report of Traffic Accident Occurring in California (SR-1) with the DMV within 10 days. [7] This filing creates a record independent of what the rideshare company or its insurer reports.

What Are the Deadlines for Filing a Rideshare Injury Claim in California?

California imposes strict deadlines on personal injury claims, and rideshare cases are not exempt. Missing a deadline can permanently bar your ability to recover compensation, regardless of how strong your case might be.

The general statute of limitations for personal injury claims in California is two years from the date of injury under California Code of Civil Procedure §335.1. [8] However, several factors can shorten or toll this period:

- Claims against government entities: If a public entity or government employee contributed to the crash. For example, if a road defect on a state highway played a role, you must file an administrative claim under the California Government Claims Act within six months of the incident. [9] Failure to present this claim within six months generally bars any lawsuit against that entity.

- Minor claimants: Different rules apply when the injured person is a minor, which can extend or modify standard deadlines.

- Discovery of injury: Some injury statutes of limitations begin running when the injury is discovered rather than when it occurred, but this exception is fact-specific and not automatic.

Because rideshare crashes often involve questions about the exact date of injury, which parties bear liability, and whether any government entity is involved, it is important to understand these timelines early. Courts in the Central Justice Center in Santa Ana (which handles Orange County civil cases) and at the Stanley Mosk Courthouse in Los Angeles (where many LA County civil cases are filed) apply these deadlines strictly.

The practical takeaway: do not wait to take action. Evidence fades, witnesses become unavailable, and video footage gets overwritten. The two-year window may feel generous, but rideshare cases require investigation that takes time.

How Does California’s Comparative Fault Rule Affect a Rideshare Claim?

California follows a pure comparative fault system, meaning that if you bear some share of responsibility for the accident, your recovery is reduced by that percentage but you are not entirely barred from recovery. [10] This rule applies to rideshare cases just as it does to any civil injury claim.

In practice, rideshare insurers frequently argue that an injured party was partially at fault whether by jaywalking when struck, failing to wear a seatbelt, or contributory conduct as a driver. These arguments are a negotiating tool designed to reduce the payout. Documented evidence, including traffic camera data, crosswalk signal timing records, and independent witness accounts, can challenge inflated fault allocations.

Multiple parties can also share fault in a rideshare crash. If an Uber driver and another motorist both contributed to a collision on SR-55 near Costa Mesa, both may owe a share of the damages to an injured passenger. The total recovery available then depends on both parties’ insurance coverage and their respective fault percentages. This multi-party dynamic is one reason rideshare cases are more complex than standard two-car accidents and why injured people benefit from having someone who understands how to build a complete claim picture.

Rideshare accident lawyers can evaluate fault allocation, identify all responsible parties, and work to counter inflated comparative fault arguments with objective evidence. Without that support, insurers have a clear negotiating advantage.

How Gosuits Irvine Helps Rideshare Injury Victims in California

If you have been injured in an Uber or Lyft accident anywhere in California as a passenger, another motorist, a pedestrian, or a rideshare driver injured by someone else, a free consultation with a member of our personal injury lawyers team can help you understand your options without any pressure or obligation.

Gosuits brings more than 30 years of combined experience handling personal injury cases across California, Texas, and Illinois. We practice in Irvine and serve clients throughout Orange County and greater Los Angeles. Our team handles cases involving rideshare accidents and wrongful death claims arising from those accidents, as well as a full range of other vehicle collision and injury matters.

What sets Gosuits apart is our commitment to technology-driven case management. We use proprietary software developed specifically for our firm that accelerates case handling, streamlines communication with insurance adjusters and opposing counsel, and gives our attorneys a clearer picture of each client’s damages at every stage of the case. Despite this technological approach, every client has a designated attorney not a case manager who has direct and unfettered access to them. You will know who is working on your case and be able to reach them directly.

Our attorneys have trial experience. That matters in rideshare cases, because insurers know whether the firm on the other side of the table is willing to take a case to verdict. A history of going to trial and achieving results changes how insurance companies evaluate your claim. You can review our prior cases to see examples of the work our team has done for clients in California and across our practice areas.

We serve clients throughout California, Texas, and Illinois, including across the Los Angeles metro area, Orange County, and the Irvine corridor. Our our attorneys page provides background on the lawyers who will handle your case, and our about us page describes the firm’s history and approach. Our full range of practice areas is available at practice areas.

We do not charge attorney fees unless we recover for you. A consultation costs you nothing. If you or someone you care about has been injured in a rideshare accident in Irvine, Los Angeles, or anywhere in Southern California, we encourage you to schedule a free consultation with our team today.

References / Resources

- California Public Utilities Code §5433 – TNC Insurance Requirements – California Legislative Information

- Transportation Network Companies – California Public Utilities Commission

- California Insurance Code §11580.1(b) – Minimum Liability Requirements – California Legislative Information

- California Insurance Code §11580.2 – Uninsured Motorist Coverage – California Legislative Information

- California Insurance Code – Stacking and Coordination Rules – California Legislative Information

- Request a Collision Report – California Highway Patrol

- Traffic Accident Reporting Requirements – California DMV

- Code of Civil Procedure §335.1 – Personal Injury Statute of Limitations – California Legislative Information

- Government Claims Program – California Department of General Services

- Civil Code §1431.2 – Comparative Fault – California Legislative Information

- Traffic Safety Data and Fatality Analysis – National Highway Traffic Safety Administration

- California Fair Claims Settlement Practices Regulations – California Department of Insurance