- What is a reservation of rights letter in an insurance dispute?

- How does a reservation of rights affect duty to defend and indemnity?

- What conflicts of interest can arise and when can you choose independent counsel?

- How should you respond to a reservation of rights letter?

- What investigation and adjuster tactics happen after a reservation of rights letter?

- How do Texas, California, Illinois, and federal courts approach reservation of rights disputes?

- What policy language and evidence drive coverage decisions after defense?

- What deadlines apply and what if the insurer delays or denies?

- How does a reservation of rights letter shape settlement strategy in personal injury litigation?

- Frequently asked questions about reservation of rights letters

- About GoSuits

- References and resources

What is a reservation of rights letter in an insurance dispute?

A reservation of rights letter is a written notice from an insurer that it will investigate and possibly defend a claim while reserving the right to contest coverage later. In plain terms, the insurer is saying it will step in for now but may later decline to pay for a judgment or settlement if it concludes the claim is not covered under the policy. The letter typically lists policy provisions and exclusions that the insurer believes might bar coverage. In coverage law, this is often called an ROR letter. It is common in personal injury claim scenarios after a car accident, motorcycle accident, slip and fall, construction accident, or product liability dispute.

Under widely recognized insurance principles, the duty to defend is distinct from and broader than the duty to indemnify. An insurer can extend a defense while still disputing indemnity, and a reservation of rights letter is the vehicle that documents that position [1] [2] [3]. If you were involved in a California car accident or a Texas 18-wheeler crash, an ROR letter does not mean the insurer has denied your claim. It signals a potential coverage dispute and sets the stage for further investigation.

In practice, these letters often arrive when there are questions about policy exclusions or conditions, such as whether the loss was expected or intended, whether the driver was a permissive user of the vehicle, whether the accident involved a commercial truck or tractor-trailer outside the policy scope, or whether there was timely notice to the insurer. A reservation of rights letter is a serious legal document. It frames the path of litigation and settlement and may affect both the plaintiff and the defendant in a personal injury lawsuit.

National data show that personal injury litigation is a significant share of civil caseloads. State court research indicates that, while outcomes vary by jurisdiction and case type, plaintiffs prevail in a large share of tort trials, and median awards can be substantial in severe injury cases [5]. Traffic safety data also reflect the frequency and severity of roadway crashes, which fuel many liability claims and insurer investigations across the country [11]. ROR letters are common in these contexts.

How does a reservation of rights affect duty to defend and indemnity?

Understanding the difference between defense and indemnity is central to evaluating a reservation of rights letter.

What is the duty to defend and how is it triggered?

The duty to defend requires the insurer to provide a legal defense to the insured whenever the allegations potentially fall within policy coverage. Across many jurisdictions, this duty is interpreted broadly in favor of providing a defense at the outset, even if ultimate coverage is uncertain. That is why an insurer may agree to defend under a reservation of rights while it investigates or litigates coverage [2].

For example, in a Dallas car accident lawsuit alleging negligence and a pedestrian accident, a liability policy’s bodily injury coverage might be potentially implicated. If the complaint’s facts could support a covered claim, the insurer generally provides defense counsel while it evaluates exclusions or limitations.

What is the duty to indemnify and when is it decided?

The duty to indemnify concerns whether the insurer must pay a judgment or settlement. This determination typically comes after facts are developed in the underlying case. Courts often note that the duty to indemnify is narrower than the duty to defend, and it turns on the actual facts as established by verdict, admissions, or stipulations rather than only on the pleadings [3].

Can an insurer defend under reservation and still deny coverage later?

Yes. A reservation of rights letter preserves the insurer’s ability to seek a declaratory judgment in court that some or all claims are not covered, even though it initially provided a defense. Federal courts hear many declaratory judgment actions between insurers and insureds under the Declaratory Judgment Act when diversity jurisdiction or a federal question exists [4].

What does this mean for plaintiffs and defendants?

- For defendants: You may receive appointed defense counsel paid by the insurer. However, coverage could still be denied later, placing you personally at risk for a judgment. You need to understand conflicts of interest and your rights regarding independent counsel in some jurisdictions.

- For plaintiffs: An ROR letter can affect settlement leverage. If the insurer disputes coverage, it might resist settlement. But if the facts support coverage, early documentation and clear liability can help move negotiations along. For instance, in a Chicago motorcycle accident with a severe head injury or concussion, careful documentation of accident causation, policy limits, and damages can influence defense evaluation and potential settlement authority.

What conflicts of interest can arise and when can you choose independent counsel?

When an insurer defends under a reservation of rights, ethical and legal conflicts can arise. The concern is that appointed defense counsel’s litigation strategy might affect coverage. Some jurisdictions have developed rules allowing the insured to select independent counsel at the insurer’s expense under specific conditions.

When does California allow independent counsel?

California codifies the right to independent counsel in certain conflicts through Civil Code section 2860. If an insurer reserves rights on an issue that defense counsel could influence in the underlying action, the insured may be entitled to select independent counsel while the insurer pays reasonable fees. The statute sets rate guidelines, billing rules, and cooperation duties between insurer and independent counsel [6].

What about Texas?

Texas case law recognizes that conflicts can arise in a defense under reservation. While Texas does not have a statute like California’s section 2860, conflicts may justify the insured’s right to participate in counsel selection or to seek separate counsel in limited circumstances. Defense under a reservation does not automatically create a conflict, so the particular allegations and coverage issues matter. Texas courts also discuss the framework for evaluating the duty to defend based on the live pleading and the policy language, often called the eight corners approach [8].

How does Illinois approach conflict and control of the defense?

Illinois recognizes a robust duty to defend where allegations potentially fall within coverage, and courts scrutinize conflicts that arise when coverage turns on facts at issue in the liability suit. Depending on the circumstances, the insured may be entitled to counsel with undivided loyalty, and coverage litigation may proceed in a separate action. Illinois law also allows fee shifting in certain insurance disputes under section 155 of the Insurance Code when an insurer’s position is vexatious and unreasonable [9] [10].

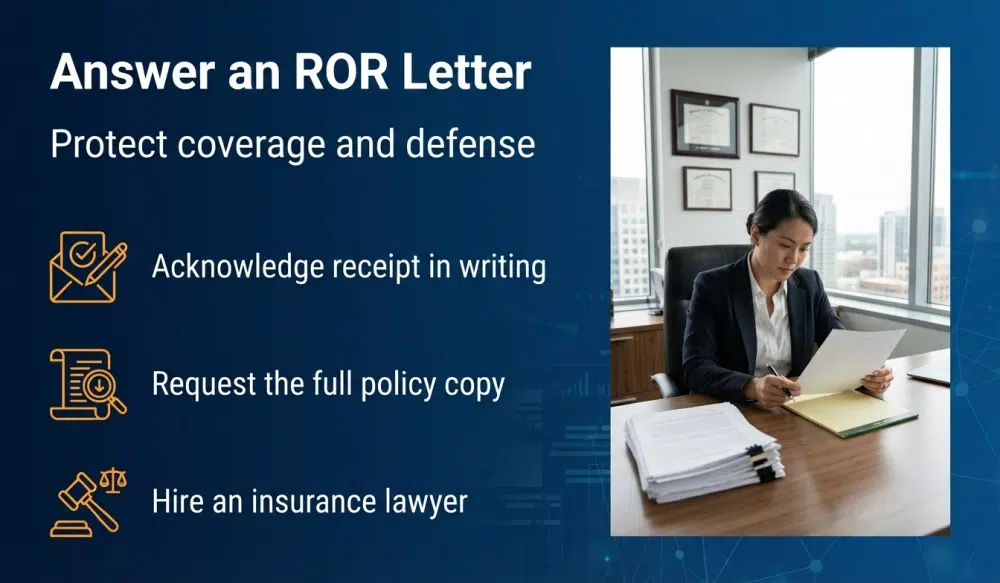

How should you respond to a reservation of rights letter?

Do not ignore an ROR letter. Your response timeline and actions can shape both coverage and the defense of the lawsuit.

What immediate steps should you take in the first 7 to 14 days?

- Calendar deadlines noted in the letter for providing information, appearing for an examination under oath, or responding to document requests.

- Acknowledge receipt in writing, confirming that you do not agree with any coverage waiver or limitation and that you are cooperating subject to all policyholder rights.

- Request the full policy if you do not have it, including endorsements and declarations pages. Ask the insurer to identify specific provisions relied upon and to clarify ambiguous allegations that supposedly trigger exclusions.

- Engage qualified coverage counsel to evaluate conflict issues, independent counsel rights, and whether to propose a defense protocol that protects you against coverage prejudice.

How should you communicate with the insurer and appointed defense counsel?

- Keep communications consistent with the duty to cooperate but avoid volunteering speculative facts that go beyond what is known. Provide documents requested that are relevant to the claim investigation.

- Protect privileged materials and agree on a protocol for sharing information between defense counsel and the insurer that does not prejudice coverage positions.

- Ask for written confirmation of defense arrangements: who is counsel, billing rates, scope of representation, and whether independent counsel is available in your jurisdiction [6].

What if there are multiple insurers or coverages?

In multi-policy situations, tender to all potentially applicable carriers promptly. For instance, a construction worksite injury might implicate commercial general liability, umbrella, or additional insured endorsements for a contractor. A serious truck crash involving a big rig or semi may trigger commercial auto coverage and excess layers. Prompt tender helps preserve defense and indemnity rights [2].

How do you navigate a personal injury claim under reservation?

Coordinate closely with your defense team. If you face a Los Angeles pedestrian accident lawsuit, or an Illinois product defect allegation involving a defective consumer product, your defense strategy should address liability and damages without conceding facts that would support a policy exclusion. Plaintiffs and defendants both benefit from timely preservation of evidence, clear documentation of injuries, and realistic settlement evaluation grounded in policy limits and coverage positions.

What investigation and adjuster tactics happen after a reservation of rights letter?

After sending an ROR letter, insurers typically escalate investigation and documentation. Understanding these steps helps you prepare.

What common requests should you expect?

- Recorded statements or examinations under oath regarding the incident timeline and policy conditions like notice and cooperation.

- Medical records and bills for a personal injury, head injury, tbi, or concussion, to assess causation and damages in car accident or motorcycle accident claims.

- Accident reports and photos from the scene of a crash, collision, slip, fall, trip, or construction scaffolding incident.

- Proof of ownership or use of a vehicle, product, property, or equipment, especially in product liability and commercial property damage matters.

What settlement and defense control issues arise?

- Defense counsel selection and strategy may be controlled by the insurer, subject to conflict rules. In California, ask whether independent counsel is appropriate under section 2860 [6].

- Settlement authority often remains with the insurer for covered claims. If coverage is disputed, settlement talks may be more complex, potentially requiring coverage counsel involvement and, sometimes, parallel declaratory relief actions [4].

- Claim handling standards are governed by unfair claims statutes and insurance regulations in many states. For example, California and Texas list prohibited claim practices. Policyholders can seek help from state insurance departments if they believe claim handling is unlawful [7] [12] [13].

How do Texas, California, Illinois, and federal courts approach reservation of rights disputes?

While core insurance concepts are similar nationwide, states apply them differently. Here are practical highlights for three major jurisdictions, with a nationwide context in federal courts.

How does California approach defense under reservation of rights?

- Independent counsel rule: If the insurer’s coverage position creates a conflict that counsel could influence in the liability case, the insured may select independent counsel at the insurer’s expense under Civil Code section 2860. The statute guides rates, fees, and cooperation [6].

- Claim practice standards: California Insurance Code section 790.03 identifies unfair claim practices, and the Department of Insurance provides consumer assistance and complaint processes [12].

- Practical note: In a California truck collision involving an 18-wheeler or tractor-trailer, conflicts can arise if coverage hinges on whether the driver acted within the scope of employment. Counsel selection and fact development should be planned with coverage in mind.

How does Texas approach defense, extrinsic evidence, and reservations?

- Defense analysis: Texas courts evaluate the duty to defend primarily by comparing the liability petition to the policy language. This is often referred to as the eight corners framework. Courts recognize limited circumstances for considering extrinsic evidence when it does not overlap with the merits [8].

- Unfair claims and prompt payment: Texas Insurance Code chapters 541 and 542 address unfair practices and prompt payment of claims, including deadlines and potential interest if an insurer delays without a valid reason [7] [13].

- Practical note: In a Texas car accident or a serious big rig crash, a reservation of rights letter often focuses on exclusions such as intentional injury, use outside the policy’s defined coverage, or late notice. Timely cooperation and carefully framed facts are crucial.

How does Illinois handle duty to defend and coverage disputes?

- Broad duty to defend: Illinois courts have repeatedly stated that if the complaint’s allegations potentially fall within policy coverage, the insurer must defend. Narrow exclusions are construed against the insurer in cases of ambiguity. When disputes over claim handling conduct arise, section 155 of the Insurance Code authorizes certain fee and penalty relief for vexatious and unreasonable conduct [9] [10].

- Practical note: In a Chicago motorcycle accident with catastrophic injury, insurers frequently reserve rights regarding exclusions and limits. Illinois courts often separate the merits case from coverage litigation to avoid prejudicing either proceeding.

What role do federal courts play?

- Declaratory judgments: Federal courts can decide coverage disputes under the Declaratory Judgment Act when jurisdictional requirements are met. Coverage questions typically rely on state insurance law, but federal procedure governs the action [4].

- Civil caseloads: The federal judiciary tracks nationwide civil filings every year. Tort cases represent a significant portion, and insurers and policyholders frequently litigate coverage in parallel with underlying claims [14].

What policy language and evidence drive coverage decisions after defense?

Key coverage outcomes often turn on the policy text and a defined set of facts learned through discovery. A structured approach helps both insureds and plaintiffs anticipate how a reservation of rights letter may evolve.

Which policy provisions are most contested?

- Insuring agreement: Defines who is insured and what counts as a covered occurrence or offense. In auto liability, look for definitions of covered vehicle and permissive user.

- Exclusions and exceptions: Intentional acts, expected or intended harm, professional liability, or product-completed operations. Some exclusions contain exceptions that restore coverage in limited scenarios [15].

- Conditions: Notice, cooperation, consent to settle, and duties after loss. Violations can support coverage defenses, but prejudice requirements vary by jurisdiction.

- Endorsements: Additional insured status, contractual liability carve outs, or special endorsements for construction or commercial trucking risks.

What evidence typically proves or defeats coverage?

- Pleadings and discovery from the underlying lawsuit, especially factual admissions about how the incident occurred.

- Accident reconstruction and witness testimony in vehicle crash or pedestrian accident litigation.

- Medical proof of injury causation and damages for personal injury, brain injury, head injury, or tbi.

- Contract and property records in construction or commercial property damage claims.

- Product design and warnings evidence in defective product cases, considering both liability and policy exclusions.

How does this apply in real world examples?

- Auto and motorcycle: An insurer may reserve rights if the at-fault driver in a Los Angeles motorcycle accident was allegedly using a vehicle without permission or engaged in intentional misconduct. Evidence about permission and intent will shape indemnity.

- Truck and tractor trailer: In a Texas crash involving a semi or big rig, disputes often focus on interstate commercial use, driver employment, and whether the tractor-trailer was scheduled on the policy.

- Slip and fall: A retailer facing a trip and fall claim in Illinois may see a reservation regarding notice or a prior known condition exclusion. Store logs, maintenance records, and surveillance video become critical.

- Construction accident: A general contractor may receive a reservation on additional insured status tied to a subcontract with a scaffold clause. The endorsement and subcontract terms can decide duty to defend for the worksite incident.

- Product liability: A manufacturer sued over a defective product might face an exclusion for known defects or recall costs, but still receive a defense for bodily injury claims.

What deadlines apply and what if the insurer delays or denies?

Deadlines arise from both policy conditions and state statutes. Missing them can harm your rights.

What prompt payment and unfair claim practice rules may apply?

- Texas: Chapters 541 and 542 of the Texas Insurance Code address unfair claim practices and prompt payment timetables in many first party contexts. While many reservation of rights disputes involve liability coverage and the duty to defend, these statutes provide timelines and remedies that can intersect with coverage investigations and settlement funds in some settings [7] [13].

- California: California Insurance Code section 790.03 lists unfair claim practices standards. The Department of Insurance offers consumer help and a complaint process if claim handling appears improper [12].

- Illinois: Section 155 of the Insurance Code allows attorney’s fees and other relief for unreasonable and vexatious delay in insurance disputes, including certain liability coverage battles [10].

What should you do if the insurer’s position stalls your case?

- Document delays and ask for written status updates with clear timelines for the claim investigation.

- Seek mediation or early neutral evaluation in both the underlying case and any coverage dispute. Federal and state courts support alternative dispute resolution to resolve contested issues efficiently [16].

- Consider declaratory relief to resolve key coverage questions that impede settlement, where appropriate jurisdiction exists [4].

- Contact your state insurance regulator if claim handling appears unlawful or unreasonably delayed. Consumer complaint portals exist in California, Texas, and Illinois to help policyholders navigate disputes [12] [13] [9].

How does a reservation of rights letter shape settlement strategy in personal injury litigation?

Settlement dynamics change when coverage is disputed. Plaintiffs and defendants must account for risk on both liability and coverage.

How should plaintiffs approach settlement when coverage is uncertain?

- Build the record to support covered theories of liability. For example, in a California pedestrian accident, emphasize negligence and covered occurrences rather than intentional conduct that may be excluded.

- Understand policy limits and endorsements. Demonstrate how alleged facts fit within insured risks to encourage the insurer to fund settlement.

- Use ADR to create a structured forum for both defense and coverage stakeholders to evaluate risk together [16].

How should defendants protect themselves during settlement talks?

- Align defense strategy with coverage preservation. Avoid stipulations that concede excluded conduct unless absolutely necessary.

- Seek independent counsel where permitted when a conflict could affect coverage, such as in California under section 2860 [6].

- Preserve contribution rights among multiple insurers and policy layers, especially in severe injury or wrongful death cases.

Serious injury litigation often features overlapping issues. In a Houston truck collision with a pedestrian, where injuries are fatal, wrongful death damages and policy stacking questions can intensify settlement pressure. Similarly, in an Illinois construction scaffold fall, additional insured endorsements and indemnity agreements can drive defense positions and settlement thresholds. Effective resolution requires coordination between defense counsel, coverage counsel, and the claims representatives controlling settlement authority.

How GoSuits Personal Injury Lawyers Can Help You

Insurance disputes often surface after a personal injury, whether from a vehicle crash, a motorcycle accident, a semi or big rig collision, a pedestrian accident, a slip or trip and fall, a construction worksite injury, a defective product incident, or a commercial property damage loss. If you received a reservation of rights letter, the next steps can affect both your defense and any settlement. A free consultation with a personal injury lawyer can clarify your path, including how to respond to a reservation of rights letter, request independent counsel where available, and align negotiation strategy with policy limits and exclusions.

GoSuits represents injury victims and families nationwide with a focus on California, Texas, and Illinois courts, and we routinely coordinate with local counsel where required. We use a technology driven approach that integrates litigation analytics with our exclusive proprietary software to move cases faster and with better organization from intake through trial. We pair advanced tools with traditional advocacy. Every client works directly with a designated trial attorney, not a case manager, and has unfettered access to their lawyer for strategy and updates.

Our team has 30 years of combined experience handling jury trials and complex settlements. Trial readiness matters in insurance disputes because it strengthens your leverage in coverage and settlement dialogues. Our past results for clients include significant outcomes in cases arising from car crashes, 18-wheeler collisions, motorcycle injuries, construction accidents, and product liability matters. See our track record at prior cases, learn about the trial team at our attorneys, and explore our full practice areas. For more on who we are and how we work, visit about us.

If you are facing a reservation of rights insurance dispute after a car accident or other personal injury, we invite you to reach out for a free consultation. We can review the ROR letter, your policy, and the lawsuit, and we will outline practical next steps to protect your rights and position your case for a fair result.

References and resources

- Reservation of rights – Cornell Law School Legal Information Institute

- Duty to defend – Cornell Law School Legal Information Institute

- Indemnity – Cornell Law School Legal Information Institute

- 28 U.S.C. 2201 Declaratory judgments – Cornell Law School Legal Information Institute

- Civil Bench and Jury Trials in State Courts, 2005 – Bureau of Justice Statistics

- Cal. Civil Code § 2860 Independent counsel in insurance defense – California Legislative Information

- Texas Insurance Code Chapter 541 Unfair Methods of Competition and Unfair or Deceptive Acts or Practices – Texas Legislature Online

- Supreme Court of Texas official website opinions and resources – Supreme Court of Texas

- Consumer Insurance Complaints – Illinois Department of Insurance

- 215 ILCS 5/155 Attorney’s fees and penalties – Illinois Compiled Statutes

- 2023 Traffic Fatalities First Three Quarters Estimate – National Highway Traffic Safety Administration

- Cal. Insurance Code § 790.03 Unfair methods and practices – California Legislative Information

- Texas Insurance Code Chapter 542 Processing and Payment of Claims – Texas Legislature Online

- Statistics and Reports – Administrative Office of the U.S. Courts

- Exclusion clause – Cornell Law School Legal Information Institute

- Alternative Dispute Resolution in the Federal Courts – Administrative Office of the U.S. Courts