- What does a personal injury settlement payment cover and who pays?

- How does the settlement payout process work from signed release to check?

- How long does the settlement check timeline usually take in the United States?

- How are attorney fees and costs deducted from the settlement?

- What are medical liens and subrogation and how do they affect your net settlement?

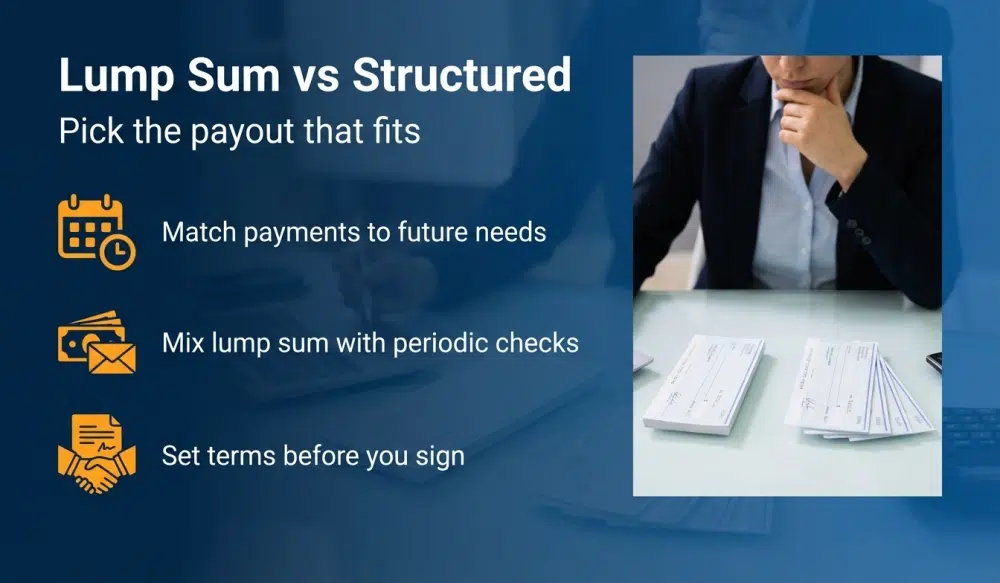

- Lump sum vs structured settlement, which payout option fits your situation?

- What are the tax implications of injury settlements?

- How do defendants and insurers handle disbursement and closing the claim?

- How do you calculate your net settlement?

- Frequently asked questions about insurance settlement disbursement

- About GoSuits

- References and resources

What does a personal injury settlement payment cover and who pays?

In a typical personal injury case in the United States, the settlement represents an agreed payment from the defendant or an insurer to resolve civil claims for losses such as medical bills, lost earnings, property damage, and non economic harms like pain and suffering compensation. Most cases settle before trial, and empirical studies of civil court systems show trials are uncommon relative to filings, with only a small fraction of civil tort disputes reaching a verdict [15]. A settlement usually ends the case in exchange for a release of all claims, which permanently closes your right to sue the same parties for the same incident. After both sides sign the release, the payer issues funds to your attorney for processing and distribution.

Common payers include auto liability insurers in a car accident or pedestrian accident, commercial insurers in a product liability case, premises insurers after a slip or fall, and general contractors or insurers after a construction incident. Severe trauma, such as a concussion or TBI from a motorcycle accident or a crash with a semi, 18-wheeler, big rig, or tractor-trailer, can involve higher medical costs and complex lien issues. Families pursuing wrongful death claims may also receive settlements that resolve all civil liability for a fatal incident.

How does the settlement payout process work from the signed release to the check?

The release is the written agreement that finalizes the settlement. You promise not to pursue any additional claims arising from the incident, and the defendant or insurer promises to pay the settlement amount. Because it permanently closes your rights, you and your attorney should review every clause carefully, especially indemnity language, Medicare or Medicaid reporting terms, and confidentiality provisions. The specific scope of claims that you release can influence tax treatment and lien responsibilities later in the process [1].

What happens to the settlement check when it arrives?

When the insurer issues payment, the settlement check is usually made payable to you and your law firm. The check is deposited into an attorney trust account, sometimes called an escrow account, and held until it clears. Under professional conduct rules, lawyers must promptly notify clients upon receiving settlement funds and safeguard those funds separate from firm assets [11] [12]. After the check clears, your lawyer calculates deductions for attorney fees under the contingency fee agreement, reimbursable case costs, and any known lien or subrogation claims. Your lawyer then provides a detailed settlement statement for your approval before disbursing your net settlement.

What is an attorney trust account or escrow account?

An attorney trust account is a bank account used exclusively to hold client funds. State rules require lawyers to keep settlement proceeds separate, keep accurate records, and deliver funds at the conclusion of the matter. For example, Texas Rule 1.14 and California Rule 1.15 require safekeeping of client property and prompt distribution once the lawyer resolves any disputed claims on the funds [11] [12]. If there is a dispute over a hospital lien or a Medicare lien amount, the disputed portion remains in the trust account until resolved, and the undisputed portion may be released to you.

How long does the settlement check timeline usually take in the United States?

There is no universal deadline for third party liability settlements, but most cases follow a similar cadence:

- Week 0 Both sides sign the release of all claims and any settlement forms, including W 9 or medical authorization if requested.

- Week 1 to 3 The insurer processes the payment request and issues the settlement check. Mail time and internal processing can extend this period.

- Bank clearance Your lawyer deposits the check into the attorney trust account. Clearance typically takes a few business days.

- Lien resolution Your lawyer confirms final balances and negotiates with lienholders and providers. Medicare or Medicaid verification can add time [4].

- Final accounting You receive a settlement statement that itemizes attorney fees, costs, medical liens, and your net settlement for approval and disbursement.

Delays often arise while obtaining final lien amounts. Medicare conditional payment information and Medicare Set Aside issues in certain contexts can require coordination with federal recovery contractors under the Medicare Secondary Payer program [4] [5]. Medicaid agencies also have statutory rights that must be addressed before disbursement [6].

What timeline considerations apply in California, Texas, and Illinois?

- California Lawyers must promptly notify and deliver funds to clients, keep funds in trust pending resolution of third party claims, and follow detailed recordkeeping under Rule 1.15 [12]. Hospital liens may affect timing until resolved under the California Civil Code Hospital Lien Act [14].

- Texas Lawyers must safeguard funds in trust, notify clients on receipt, and promptly deliver undisputed sums while holding disputed amounts until resolved under Rule 1.14 [11]. Hospital liens under Texas Property Code Chapter 55 may require confirmation and negotiation before disbursement [13].

- Illinois While third party insurance payment deadlines vary, healthcare liens are governed by the Health Care Services Lien Act, which can shape how much is paid to providers before releasing the remainder to you [15].

Local practices vary, but a practical settlement check timeline often ranges from two to eight weeks after signing the release, depending on lender verification, lienholder response times, and whether you have Medicare or Medicaid coverage.

How are attorney fees and costs deducted from the settlement?

Contingency fee agreements are common in personal injury representation. Under a contingency agreement, you pay attorney fees only if there is a recovery. State rules typically require a written agreement that explains the fee percentage, what happens if the case goes to trial, and how litigation costs will be handled. For example, Texas Rule 1.04 requires a written agreement for contingent fees and disclosure of the method by which the fee is to be determined, including percentages that accrue in the event of settlement, trial, or appeal, and whether expenses are deducted before or after the fee is calculated [11]. You should receive a closing statement showing the outcome and the remittance to you.

What litigation costs can be reimbursed?

Reimbursable costs vary by case and agreement, but often include:

- Medical records and billing retrieval fees and certified copies

- Filing fees and service of process if suit was filed

- Depositions and transcripts for witnesses or treating providers

- Expert witness work such as accident reconstruction in a collision involving a truck or a crash causing a head injury, or product defect analysis in a defective product case

- Investigation and travel expenses that are case-related

Your agreement should explain whether costs are deducted before calculating the fee or after. That choice changes your net settlement.

What are medical liens and subrogation and how do they affect your net settlement?

Liens and subrogation rights determine who must be paid from your settlement before you receive the net amount. They arise from statutes, contracts, and court decisions. Resolving them correctly is essential, because government payers and private plans can pursue recovery after settlement if their interests were ignored.

How do Medicare lien and Medicaid lien work?

- Medicare Secondary Payer If Medicare paid conditionally for your accident related care, federal law requires reimbursement from your settlement. The Centers for Medicare and Medicaid Services administers recovery under the Medicare Secondary Payer program [4]. The statutory basis is 42 U.S.C. 1395y, which obligates primary plans like liability insurance to pay before Medicare and allows the government to recover conditional payments plus interest [5].

- Medicaid rights and limits Federal Medicaid law contains an anti lien provision that protects a beneficiary’s property, with important Supreme Court decisions clarifying that states can recover only from the portion of a settlement allocated to medical expenses. Arkansas Department of Health and Human Services v. Ahlborn and Wos v. E.M.A. hold that states cannot broadly attach non medical damages like pain and suffering [6] [7] [8].

Practical steps include verifying conditional payments, disputing unrelated charges, and documenting the medical allocation of your settlement if appropriate. Your lawyer may hold funds in trust until final Medicare or Medicaid statements are received.

How do ERISA health plan lien and private insurer subrogation work?

Employer sponsored health plans governed by ERISA often include reimbursement or subrogation clauses, allowing the plan to recover from your settlement. The Supreme Court has recognized the enforcement of equitable liens by agreement under ERISA plan terms, which typically allows a plan to seek repayment from settlement funds in your possession [9]. The specific language of your plan, plus any state law limits that are not preempted by ERISA, will guide the negotiation. Private non ERISA policies and medical payments coverage may also claim a right of reimbursement under state statutes or contract terms.

What about hospital liens, letters of protection, and provider balances?

- Hospital liens Many states allow hospitals to file statutory liens to secure payment from third party settlements. For instance, Texas Property Code Chapter 55 permits hospital and emergency services liens in certain conditions [13], and California’s Hospital Lien Act governs similar claims [14]. Illinois has the Health Care Services Lien Act that sets caps and notice requirements [15].

- Letters of protection Some providers agree to delay collection and treat on credit in exchange for a letter of protection, which promises payment from any settlement. LOPs are negotiated documents, not universal forms, and their terms vary by provider and jurisdiction.

- Negotiations Your attorney can dispute unrelated billing, reduce balances, and apply statutory caps. Negotiation outcomes directly affect your net settlement.

What is a structured annuity and how is it arranged?

A structured settlement spreads payments over time using an annuity. Federal tax law supports tax favored treatment of periodic payments for personal physical injuries and allows qualified assignments of the liability to an annuity issuer under Internal Revenue Code section 130 [3]. When the structure is correctly arranged at the time of settlement, the periodic payments for personal physical injuries are generally excluded from taxable income under section 104(a)(2) [2]. Because a structure must be set up before you sign the release, speak with your attorney about timing. Structured payments can address long term care after a head injury or brain trauma, fund predictable therapy after a worksite fall from a scaffold, or create college funds in a wrongful death case for surviving children.

Can you combine lump sum and periodic payments?

Yes. Many settlements use a hybrid approach. A lump sum can pay liens, fees, and immediate bills, while a structured annuity delivers predictable tax favored payments for future needs [2] [3]. Defendants and insurers work with structure brokers to finalize annuity terms. Once in place, a structure is typically irrevocable. Evaluate inflation, cost of living adjustments, and guaranteed periods against your budget and risk tolerance.

What are the tax implications of injury settlements?

For personal physical injuries or physical sickness, the Internal Revenue Code generally excludes compensatory damages from gross income, whether paid in a lump sum or through periodic structured payments [2]. The IRS provides consumer guidance in Publication 4345 addressing when settlements are taxable or nontaxable [1]. The exclusion does not apply if there is no physical injury or sickness.

What parts can be taxable such as lost wages, interest, and punitive damages?

- Punitive damages are taxable, even if related to a physical injury, unless a narrow statutory exception applies that is rarely relevant in ordinary personal injury cases [1].

- Prejudgment or post judgment interest is generally taxable [1].

- Emotional distress damages without a physical injury are taxable, though related medical costs may be deductible subject to limitations [1].

Attorney fees can have tax consequences depending on the nature of the claims. In most physical injury cases, the exclusion applies to the full recovery, which typically avoids separate taxation on the portion paid to your attorney. Discuss your specific facts with a qualified tax professional before finalizing a settlement allocation.

How do taxes differ in California, Texas, Illinois?

States may conform to federal rules or have additional provisions. California generally conforms to the federal exclusion for personal physical injuries in the state income tax base, while Texas does not impose a state income tax. Illinois generally conforms to federal definitions with state modifications. Because the details can change, it is prudent to confirm current state tax treatment before disbursement.

How do defendants and insurers handle disbursement and closing the claim?

Insurers require executed releases, final W 9 forms, and sometimes lien affidavits before issuing settlement checks. In cases involving Medicare, payers may report settlements to CMS under the Medicare Secondary Payer reporting rules. If your case involved a vehicle collision or a defective product, the insurer may also require proof that all known lienholders have been addressed before closing the file. For bicycle or motorcycle accident matters or a tractor-trailer crash, commercial insurers may use structured settlement professionals to price periodic payment streams. Once checks are cut and mailed, your law firm processes the funds through the attorney trust account consistent with professional rules [11] [12].

What documents should you review before authorizing disbursement?

- Settlement statement itemizing all deductions and your net settlement

- Final lien statements for Medicare, Medicaid, ERISA plans, and hospitals

- Provider releases for balances covered by letters of protection

- Trust account ledger showing deposit and disbursements consistent with state rules [11] [12]

How GoSuits Personal Injury Attorneys Can Help You

When you have questions about how personal injury settlements are paid, it can feel overwhelming to sort through insurance terms, releases, Medicare rules, and lien laws. A free consultation with a personal injury attorney at GoSuits helps you understand your options, the settlement payout process, and what to expect in your specific case. We represent clients across the United States.

We built GoSuits on a technology driven approach. Our exclusive proprietary software streamlines evidence collection, claim valuation, and lien resolution so cases move faster with better organization. We combine innovation with direct attorney attention. Although we use advanced tools to expedite your case, we assign a designated attorney to every client. We do not use case managers for legal work, and you have unfettered access to your attorney for updates and strategy.

Our team brings 30 years of combined experience in civil litigation, including trials in state and federal courts. Trial experience matters because it informs case strategy, negotiation posture, and preparation from day one. We have obtained meaningful results for clients in a range of matters, from a car accident or pedestrian crash to complex product liability and wrongful death claims. You can explore a sample of our prior cases, meet our attorneys, learn more about us, and review our full practice areas.

Our practice includes personal injury, car accident and vehicle collisions, motorcycle claims, truck and tractor-trailer crashes, slip and fall matters, construction incidents, brain and head injury cases, product liability, commercial property damage disputes, and wrongful death claims. Whether your case involves a trip hazard at a worksite, a scaffold failure, a defective product, or a fatal crash, we focus on careful preparation and clear communication so you can make informed decisions at every step.

References and resources

- Publication 4345, Settlements Taxability – Internal Revenue Service

- 26 U.S.C. 104 Exclusion from gross income – Legal Information Institute

- 26 U.S.C. 130 Certain personal injury liability assignments – Legal Information Institute

- Medicare Secondary Payer Overview – Centers for Medicare and Medicaid Services

- 42 U.S.C. 1395y Medicare Secondary Payer – Legal Information Institute

- 42 U.S.C. 1396p Medicaid anti lien provisions – Legal Information Institute

- Arkansas Dept. of Health and Human Services v. Ahlborn – Legal Information Institute

- Wos v. E.M.A. – Legal Information Institute

- Sereboff v. Mid Atlantic Medical Services, Inc. – Legal Information Institute

- Texas Disciplinary Rules of Professional Conduct including Rules 1.04 and 1.14 – Supreme Court of Texas

- California Rule of Professional Conduct 1.15 Safekeeping Funds – State Bar of California

- Texas Property Code Chapter 55 Hospital and Emergency Services Liens – Texas Legislature Online

- California Civil Code Sections 3045.1 to 3045.6 Hospital Lien Act – California Legislative Information

- 770 ILCS 23 Health Care Services Lien Act – Illinois General Assembly

- Civil Bench and Jury Trials in State Courts, 2005 – Bureau of Justice Statistics