- What is a Travelers accident claim and when should you report it?

- What immediate steps should you take after a crash before you file with Travelers?

- Which documents do you need to start a Travelers car insurance claim?

- How do you file a Travelers auto accident claim online, by phone, or in-app?

- What are the Travelers claim process steps from first notice to payout?

- How do fault and comparative negligence rules affect your Travelers settlement?

- What are the deadlines to file car accident claims in Texas, California, and Illinois?

- How do medical bills and liens work after a car crash covered by Travelers?

- What if the other driver is uninsured or underinsured and you have Travelers UM or UIM?

- How do you negotiate a Travelers settlement without hurting your case?

- Why do insurers deny or delay claims and what are your options?

- When can a denied Travelers claim become a bad faith insurance claim?

- How do lawsuits interact with a pending Travelers claim?

- What should defendants and insured drivers know about a Travelers defense?

- How do property damage claims with Travelers differ from injury claims?

- What are common mistakes to avoid when dealing with Travelers adjusters?

- How can you contact Travelers claims and where do you find the phone number?

- Are there special considerations in Houston, Dallas, Austin, San Antonio, and Fort Worth?

- What should Los Angeles, San Diego, Orange County, San Francisco, and Sacramento drivers know?

- How do Chicago, Naperville, Aurora, and Joliet cases often play out?

- How can GoSuits help with a Travelers accident claim?

- Authoritative resources

What is a Travelers accident claim and when should you report it?

A Travelers accident claim is a request for benefits under a Travelers Insurance auto policy after a crash. You might file a Travelers car insurance claim for your own injuries or property damage if you are insured by Travelers, or you might present a third-party claim against a Travelers policy if their insured driver caused your losses.

Timely reporting matters. Many policies require prompt notice and cooperation. Delayed reporting can complicate fault investigations, witness memory, and documentation. Nationally, motor vehicle crashes remain a serious public safety and economic issue. The National Highway Traffic Safety Administration reports 42,514 traffic fatalities in 2022 and estimates the economic cost of crashes at $340 billion for 2019, including medical costs, lost productivity, property damage, and congestion [NHTSA 2022 fatalities] and [NHTSA Economic Impact 2019]. These figures highlight why acting quickly to protect your claim is important.

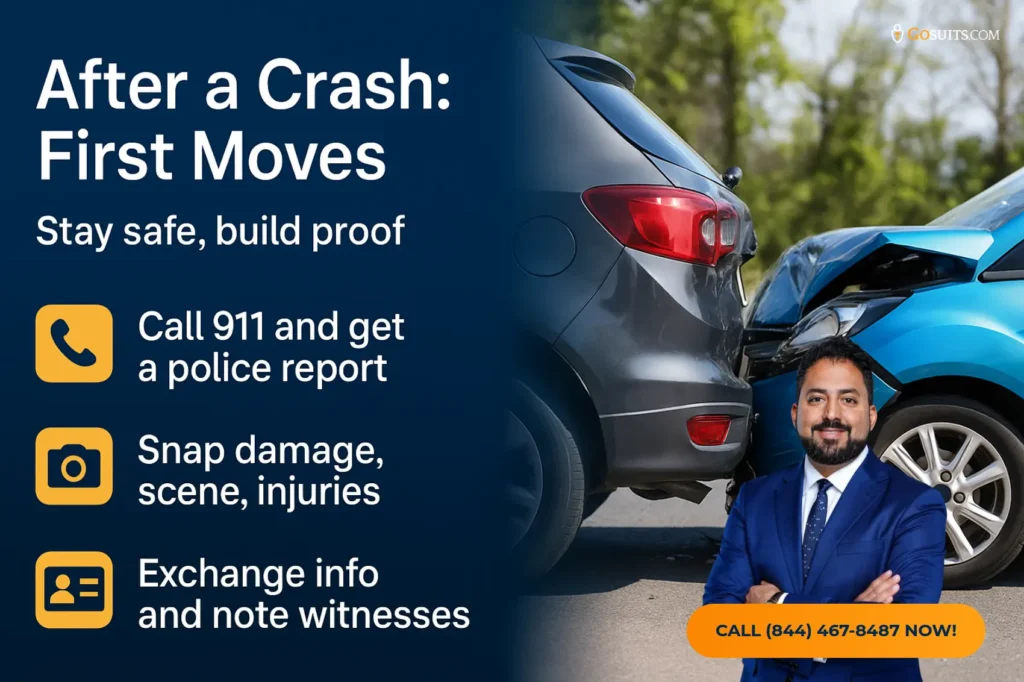

What immediate steps should you take after a crash before you file with Travelers?

Your safety comes first. If you can, move to a safe area and call 911. Collect information and evidence that will help your Travelers accident claim or defense if you are accused of causing the crash.

- Call police and seek medical care. A police report and prompt evaluation create objective records. Emergency services guidance is available through local authorities, and national data show early treatment can reduce severity of outcomes in crashes [NHTSA Trauma Systems].

- Exchange information. Share names, contact details, driver’s license numbers, plate numbers, and insurance information with all involved drivers and note any passengers and witnesses.

- Document the scene. Photograph vehicle positions, damage, debris, skid marks, traffic controls, and weather. Save dashcam footage if available.

- Preserve evidence of injuries. Keep copies of discharge papers, prescriptions, imaging, and follow-up instructions.

- Avoid detailed statements at the scene. Keep communications factual. Do not speculate on fault.

Which documents do you need to start a Travelers car insurance claim?

Having the right documentation helps Travelers verify coverage and evaluate liability and damages.

- Proof of insurance and policy number. Your Travelers ID card or declarations page.

- Police report information. Agency name, report number, and officer contact details.

- Photos and videos. Crash scene, vehicle damage, and visible injuries.

- Medical records and bills. ER records, physician notes, therapy plans, invoices, pharmacy receipts. These establish causation and value of medical bills after a car crash.

- Employment documentation. Pay stubs and employer statements for lost wages.

- Property damage estimates. Body shop repair estimates, towing receipts, and rental car invoices for a Travelers property damage claim.

- Witness contacts. Names, numbers, and brief summaries of observations.

- Health insurer information. To address liens and subrogation if applicable.

How do you file a Travelers auto accident claim online, by phone, or in-app?

You can usually report a car accident to Travelers through your policy’s listed channels. If you are a third party, you can still notify Travelers of a claim against their insured. For the most accurate contact details, use the claims phone number printed on your Travelers ID card or the official Travelers website or app. Be ready with date, time, location, vehicle information, a brief description of what happened, and whether anyone was injured.

- Online or app. Filing digitally allows you to upload photos, police report numbers, and documents.

- By phone. Calling the Travelers claims phone number on your policy documents can get an adjuster assigned quickly.

- Through your attorney. If you already have counsel, your attorney can open the claim and handle communications to avoid mistakes.

What are the Travelers claim process steps from first notice to payout?

While every case is unique, most Travelers claim process steps follow a predictable path.

- First Notice of Loss. You provide basic details and contact information.

- Coverage review. Travelers checks if the policy was active, what coverages apply, and any exclusions.

- Liability investigation. Adjusters gather statements, photos, vehicle inspections, scene data, and witness contacts. In some cases, they retain accident reconstruction or consult traffic codes.

- Medical and property review. For a Travelers auto accident claim, they review medical records, bills, and vehicle estimates. They may request authorizations. Provide only what is reasonably necessary.

- Evaluation. Adjusters evaluate fault under state negligence rules and assess damages, including medical expenses, lost wages, and pain and suffering when allowed by law.

- Negotiation. You or your lawyer exchange demands and offers. Many claims resolve here.

- Payment or denial. If agreed, Travelers issues payment. If denied or undervalued, you can appeal, provide more evidence, or file suit within legal deadlines.

Most insurers seek to resolve property claims quickly and bodily injury claims after treatment stabilizes. Patience may improve documentation, but delay risks approaching statute of limitations or policy notice deadlines.

How do fault and comparative negligence rules affect your Travelers settlement?

Fault rules vary by state and affect how much you can recover.

- Texas. Texas uses modified comparative negligence. You cannot recover if you are more than 50 percent responsible, and any award is reduced by your percentage of fault [Tex. Civ. Prac. & Rem. Code § 33.001].

- California. California follows pure comparative negligence. Your recovery is reduced by your share of fault, even if you are primarily at fault [Li v. Yellow Cab Co., 13 Cal.3d 804 (1975) via Google Scholar].

- Illinois. Illinois applies modified comparative negligence with a 51 percent bar. Recovery is barred if your fault exceeds 50 percent, and otherwise reduced by your fault percentage [735 ILCS 5/2-1116].

These rules inform how Travelers evaluates liability and negotiates your settlement. Even partial fault allegations can significantly adjust offers.

What are the deadlines to file car accident claims in Texas, California, and Illinois?

Missing a statute of limitations can end your right to recover in court. Policy notice deadlines can also affect coverage. Check your Travelers policy and the following general state deadlines for civil motor vehicle cases.

- Texas. Personal injury claims generally must be filed within 2 years of the crash [Tex. Civ. Prac. & Rem. Code § 16.003]. Property damage claims also typically have a 2-year period.

- California. Personal injury claims generally have a 2-year statute [Cal. Code Civ. Proc. § 335.1], and property damage claims often have 3 years [Cal. Code Civ. Proc. § 338].

- Illinois. Personal injury claims usually must be filed within 2 years [735 ILCS 5/13-202]. Property damage is often 5 years [735 ILCS 5/13-205].

Claims against government entities usually have shorter notice requirements. Do not wait to evaluate your deadlines.

How do medical bills and liens work after a car crash covered by Travelers?

Healthcare expenses can pile up quickly. How they are handled affects your net recovery.

- Health insurance coordination. Your health insurer may pay first and later assert a lien or subrogation claim. State and federal rules govern lien rights for public programs.

- MedPay or PIP. If your Travelers policy includes Medical Payments or Personal Injury Protection, it can help cover initial medical bills after a car crash regardless of fault, subject to policy limits.

- Tax treatment. In general, compensatory damages for personal physical injuries are not taxable, but lost wages and interest may be taxable. See IRS guidance at [IRS Pub. 4345, Settlements – Taxability] and Internal Revenue Code § 104(a)(2) [Cornell Law LII].

- Medical liens. Hospitals and public programs can claim a portion of a settlement under state lien statutes. Negotiation can affect lien amounts.

Document treatment and keep all invoices. Coordinating benefits early can reduce delays at settlement time.

What if the other driver is uninsured or underinsured, and you have Travelers UM or UIM?

Uninsured and underinsured motorist coverage can protect you when the at-fault driver lacks sufficient coverage. You must generally prove the other driver’s fault and damages, just as in a liability claim. Check your policy for notice and consent-to-settle provisions. Some policies require arbitration for UM or UIM disputes. Deadlines may be set by contract in addition to state statutes, so act promptly.

How do you negotiate a Travelers settlement without hurting your case?

Negotiation is evidence-driven. A thoughtful approach helps you avoid missteps.

- Build a complete demand. Include liability summary, medical chronology, bills and records, wage loss proof, out-of-pocket costs, and any future care opinions supported by records.

- Be cautious with recorded statements. You do not have to give a recorded statement to the other driver’s insurer. If you are a Travelers insured, your policy may require cooperation, but discuss the scope before giving broad releases.

- Address comparative fault. Acknowledge weak points and explain why your share of fault is low under state rules.

- Use objective anchors. Cite diagnostic imaging, physician assessments, and functional limitations in daily activities.

- Time your demand. Demanding too early can leave out treatment or prognosis. Waiting too long risks legal deadlines.

- Protect confidentiality. Share only relevant portions of prior medical history necessary to assess causation and damages.

Why do insurers deny or delay claims and what are your options?

Denials or delays may be based on liability disputes, policy exclusions, insufficient documentation, or valuation disagreements. Each state sets standards for fair claims handling.

- Texas. Texas law prohibits unfair or deceptive insurance practices and sets prompt payment rules, including deadlines for acknowledging, investigating, and paying claims [Tex. Ins. Code ch. 541] and [Tex. Ins. Code ch. 542].

- California. The Fair Claims Settlement Practices Regulations require insurers to communicate promptly, conduct thorough investigations, and not misrepresent facts or policy provisions [10 CCR § 2695.1 et seq.].

- Illinois. The Insurance Code defines improper claims practices, including misrepresentation and failing to adopt reasonable investigation standards [215 ILCS 5/154.6].

If you experience a denial or delay, you can request written reasons, submit additional evidence, escalate to a supervisor, file a complaint with the state insurance department, or pursue litigation where appropriate.

When can a denied Travelers claim become a bad faith insurance claim?

Bad faith generally involves an insurer’s failure to act fairly and in good faith toward its insured. Standards vary by state and depend on whether the claim is first-party or third-party.

- Texas insureds. Statutory remedies exist for unfair practices and prompt payment violations, and common-law bad faith may apply in certain first-party contexts [Tex. Ins. Code ch. 541] and [Tex. Ins. Code ch. 542].

- California insureds. California recognizes tort claims for first-party bad faith when an insurer unreasonably withholds benefits due under the policy. See foundational discussions in [Gruenberg v. Aetna, 9 Cal.3d 566 (1973) via Google Scholar].

- Illinois insureds. Section 155 authorizes attorney fees and penalties for unreasonable and vexatious delay by insurers in certain cases [215 ILCS 5/155].

Third-party claimants typically cannot sue for bad faith against the other driver’s insurer, but they can pursue the at-fault driver, and in limited circumstances, assignment of rights may occur after excess judgments. Discuss your options before making decisions that could affect coverage.

How do lawsuits interact with a pending Travelers claim?

Filing a lawsuit preserves your claim when negotiations stall or the statute of limitations is approaching. The litigation process includes pleadings, discovery, motions, and trial. Some defendants remove cases to federal court when diversity jurisdiction exists and requirements are met, such as complete diversity and an amount in controversy over $75,000 [28 U.S.C. § 1332] and removal standards at [28 U.S.C. § 1441].

Even after suit is filed, most cases settle. Courts often encourage alternative dispute resolution. Your litigation strategy should account for comparative fault, available insurance limits, and liens.

What should defendants and insured drivers know about a Travelers defense?

If you are insured by Travelers and get sued, promptly forward the lawsuit to Travelers so a defense can be arranged if the claim is covered. Cooperation is usually required under your policy. You may be asked to provide statements, documents, and attend an examination under oath. Defense counsel retained by Travelers represents you. If claimed damages exceed your policy limits, you can ask about excess exposure, settlement opportunities within limits, and personal counsel to advise you on potential conflicts of interest.

How do property damage claims with Travelers differ from injury claims?

Property claims often move faster because damage is easier to quantify.

- Repair vs total loss. Adjusters compare repair costs to the actual cash value. You can submit competing estimates.

- Diminished value. Some states allow claims for reduced vehicle value after repairs, depending on policy and evidence.

- Rental and loss of use. Keep receipts for rental vehicles or document loss of use if you could not secure a rental.

- Personal property. Items damaged in the vehicle may be covered depending on the policy.

What are common mistakes to avoid when dealing with Travelers adjusters?

- Giving broad medical authorizations. Limit releases to relevant providers and time frames.

- Posting on social media. Public content may be used to dispute injury claims.

- Accepting early low offers. Quick offers might not account for future care, therapy, or lost earning capacity.

- Missing deadlines. Calendar statutes of limitations and policy notice requirements.

- Repairing vehicles before inspection. Allow Travelers or the other insurer to inspect before repairs when possible.

- Self-representation in complex cases. High-injury or disputed-fault cases benefit from legal help.

How can you contact Travelers claim,s and where do you find the phone number?

To file a Travelers claim or check status, use the claims phone number printed on your Travelers ID card, declarations page, or on the official Travelers website or app. Contact details can change, so rely on your current policy documents. If you are a third-party claimant, you can ask the at-fault driver for their Travelers policy information, including the claim number once opened.

Are there special considerations in Houston, Dallas, Austin, San Antonio, and Fort Worth?

Texas has unique procedural and substantive rules that affect a Travelers accident claim.

- Comparative fault and proportionate responsibility. Texas bars recovery if you are more than 50 percent at fault [§ 33.001]. Houston, Dallas, Austin, San Antonio, and Fort Worth collisions often involve multi-vehicle pileups where proportionate responsibility is contested.

- Two-year statute. Personal injury and property damage claims are typically two years from the accident date [§ 16.003].

- Prompt payment rules. Texas imposes timelines for acknowledging, investigating, and paying first-party claims, with potential interest penalties for delay [Texas Insurance Code ch. 542].

- Court procedures. The Texas Judicial Branch publishes rules and standards that govern civil practice statewide [Texas Courts Rules & Standards].

- Legal research help. The Texas State Law Library hosts a guide on car accidents and insurance claims with statutes and forms [Texas Law Library Guide].

What should Los Angeles, San Diego, Orange County, San Francisco, and Sacramento drivers know?

California’s legal landscape influences how Travelers evaluates claims.

- Pure comparative negligence. Your recovery is reduced by your fault share, even if you are most at fault [Li v. Yellow Cab].

- Two-year personal injury and three-year property limits. See [CCP § 335.1] and [CCP § 338].

- Fair Claims regulations. California requires timely and fair claims handling [10 CCR § 2695.1 et seq.].

- Local considerations. Congested corridors in Los Angeles, Orange County, and the Bay Area increase multi-defendant scenarios, rideshare involvement, and UM or UIM issues. Keep robust documentation.

- Court self-help. The Judicial Council offers civil self-help materials that explain timelines and procedures [California Courts Self-Help].

How do Chicago, Naperville, Aurora, and Joliet cases often play out?

Illinois rules shape negotiation and litigation strategies with Travelers.

- 51 percent bar for comparative negligence. Recovery is barred if your fault exceeds 50 percent [735 ILCS 5/2-1116].

- Deadlines. Two years for personal injury and five years for property damage in many cases [§ 13-202], [§ 13-205].

- Claims practices. Unfair claims methods are prohibited and can be investigated by regulators [215 ILCS 5/154.6].

- Urban crash patterns. Dense traffic and intersections in Chicago and suburbs often lead to disputed right-of-way and pedestrian claims. Preserve video from nearby businesses when possible.

- Court resources. Illinois Courts publish civil resources and forms [Illinois Courts].

How can GoSuits help with a Travelers accident claim?

When you face injuries, medical bills, and vehicle repairs, it is hard to manage a Travelers claim on your own. A free consultation with a personal injury lawyer can clarify fault, coverage, deadlines, and strategy. GoSuits represents clients in Texas, California, and Illinois, including Houston, Dallas, Austin, San Antonio, Fort Worth, Los Angeles, San Diego, Orange County, San Francisco, Sacramento, Chicago, Naperville, Aurora, and Joliet.

- Technology-driven from day one. We built exclusive proprietary software that organizes evidence, tracks medical records, and models damages. This helps move claims faster and present clearer, data-backed demands to insurers like Travelers.

- Leadership in innovation. Our systems integrate crash analytics, medical timelines, and lien management into one secure workspace to reduce friction and delays.

- Dedicated attorney access. Although we leverage technology to expedite the case, every client works directly with a designated attorney. We do not use case managers, and clients have unfettered access to their lawyer.

- Past results and trial readiness. We have resolved significant injury and wrongful death cases and have taken cases to verdict when needed. You can review examples of prior matters here: Prior case results and trial experience. Results depend on facts and law; past outcomes do not predict future results.

- Full-spectrum personal injury practice. We handle auto, trucking, pedestrian, bicycle, rideshare, premises, and product-related injury cases, along with uninsured and underinsured motorist claims.

- 30 years of combined experience. Our attorneys bring decades of courtroom and negotiation experience to each file, which can be critical if a Travelers claim requires suit.

- Focus on both plaintiffs’ and defendants’ dynamics. Understanding how insurers evaluate risk, reserve cases, and litigate helps us anticipate moves and build leverage.

If you have questions about a Travelers accident claim, we are here to help you understand your options, protect deadlines, and pursue the fullest recovery available under the law.

Authoritative resources

- NHTSA 2022 traffic fatalities estimate

- NHTSA Economic and Societal Impact of Motor Vehicle Crashes, 2019

- IRS Publication 4345 on settlements and taxability

- Cornell Law LII: 26 U.S.C. § 104

- Texas statute of limitations for injury and property damage

- Texas comparative negligence rule

- Texas Insurance Code chapter 541

- Texas Insurance Code chapter 542

- Texas Courts Rules and Standards

- Texas State Law Library Car Accidents Guide

- California Code of Civil Procedure § 335.1

- California Code of Civil Procedure § 338

- Li v. Yellow Cab Co. of California, 13 Cal.3d 804 (1975)

- California Fair Claims Settlement Practices Regulations

- 735 ILCS 5/13-202 Illinois PI statute of limitations

- 735 ILCS 5/13-205 Illinois property statute of limitations

- 215 ILCS 5/154.6 Unfair claims practices

- 215 ILCS 5/155 Remedies for unreasonable and vexatious delay

- Illinois Courts

- California Courts Self-Help

- 28 U.S.C. § 1332 diversity jurisdiction

- 28 U.S.C. § 1441 removal