- What is an ERISA lien and why does it impact your personal injury settlement?

- How does ERISA subrogation and reimbursement actually work in practice?

- Is your health plan self-funded or insured, and why does that matter for ERISA liens?

- What is ERISA preemption and how can it override state subrogation laws?

- Which U.S. Supreme Court cases control ERISA reimbursement rights?

- Do the make-whole and common fund doctrines reduce ERISA liens?

- What documents should you request from the plan administrator to audit an ERISA lien?

- How can you negotiate or reduce an ERISA health insurance lien?

- How do you calculate a potential ERISA lien reduction step by step?

- How should defendants and insurers handle ERISA liens during settlement?

- How do ERISA liens interact with Texas law in Houston, Dallas, Austin, and San Antonio?

- How do ERISA liens interact with California law in Los Angeles, San Diego, San Francisco, Sacramento, and Orange County?

- How do ERISA liens interact with Illinois law in Chicago, Springfield, and Naperville?

- Do ERISA liens apply to wrongful death or loss of consortium claims?

- What happens if the settlement funds are spent before an ERISA plan seeks reimbursement?

- What other frequently asked questions come up about ERISA liens near me in TX, CA, and IL?

- How can GoSuits help you navigate ERISA liens with a technology-forward personal injury practice?

- Where can you find official, trustworthy resources about ERISA liens and subrogation?

What is an ERISA lien and why does it impact your personal injury settlement?

If your medical bills after a car crash or other injury were paid by an employer health plan, that plan may seek money back from your personal injury settlement. This claim is often called an ERISA lien, ERISA subrogation, or health plan reimbursement. The federal law behind it is the Employee Retirement Income Security Act of 1974, better known as ERISA. It allows a plan fiduciary to bring a civil action for appropriate equitable relief to enforce the terms of the plan, including a reimbursement provision, under 29 U.S.C. § 1132(a)(3) [LII].

Because ERISA is federal law, it can supersede conflicting state insurance or lien laws when the plan is self-funded. The plan’s reimbursement rights are usually spelled out in the plan document and the summary plan description. If repayment is required, the plan may have first-dollar priority to your settlement, meaning it can seek to be paid before you receive any portion of the recovery, subject to defenses and case law discussed below.

ERISA liens matter because they can significantly reduce the net amount you take home. The earlier you identify whether an ERISA plan is involved, the better positioned you are to address it, request the controlling documents, and evaluate opportunities to reduce or resolve the lien.

Health coverage is common. The U.S. Census Bureau reports that in 2022, 54.5 percent of people had employment-based health insurance coverage [U.S. Census]. If you are covered through your job in Texas, California, or Illinois, odds are high that an ERISA plan may be involved in your medical payments after an injury.

How does ERISA subrogation and reimbursement actually work in practice?

Most ERISA health plans include subrogation or reimbursement language. Subrogation allows the plan to step into your shoes to pursue recovery against a third party responsible for your injuries. Reimbursement requires you to pay the plan back out of any settlement or judgment you receive from that third party. Plans typically prefer reimbursement because it is contract-based and enforced through federal equitable claims under ERISA.

When a settlement is anticipated, the plan or its recovery vendor usually sends notice of a lien. The plan may request information about the claim, the at-fault party, liability coverage, and your attorney. Once the claim resolves, the plan seeks repayment from the recovery funds held by your lawyer. Many plans attempt to assert first-priority rights to settlement funds. Whether that position holds depends on the wording of the plan documents and controlling federal case law.

Is your health plan self-funded or insured, and why does that matter for ERISA liens?

Whether a plan is self-funded or insured often determines how strong the ERISA lien is and whether state law limits apply.

- Self-funded ERISA plan means the employer pays claims from its own assets. These plans are broadly protected by ERISA preemption and are not treated as insurers for state law purposes. The Supreme Court explained this in FMC Corp. v. Holliday, 498 U.S. 52, 61–65, holding that state anti-subrogation laws cannot be applied to self-funded ERISA plans because of the deemer clause [LII FMC] and 29 U.S.C. § 1144(b)(2)(B) [LII §1144].

- Insured ERISA plan means the employer buys a group insurance policy. The policy is subject to state insurance regulation through ERISA’s savings clause, 29 U.S.C. § 1144(b)(2)(A). As a result, state statutes limiting health insurance reimbursement may apply to the insurer’s lien rights. The plan itself remains governed by ERISA, but the insurance aspects are regulated by state law [LII §1144].

To find out your plan’s funding status, request the plan document and summary plan description from the plan administrator and ask for the most recent Form 5500 filing. Many plans file a Form 5500 with the U.S. Department of Labor that shows whether health benefits are fully insured or funded through a trust. The Department of Labor maintains Form 5500 resources and search information [DOL EBSA Form 5500]. If a plan is governmental or a church plan, it may be exempt from ERISA’s subchapter I under 29 U.S.C. § 1003(b) [LII §1003].

What is ERISA preemption and how can it override state subrogation laws?

ERISA includes a broad preemption clause: state laws that relate to employee benefit plans are generally preempted, 29 U.S.C. § 1144(a) [LII §1144]. There are two key carve-outs:

- Savings clause saves state laws that regulate insurance from preemption, § 1144(b)(2)(A).

- Deemer clause prevents states from deeming an employee benefit plan to be an insurer, § 1144(b)(2)(B). This is why self-funded plans are not subject to state insurance limits on subrogation, as confirmed in FMC Corp. v. Holliday [LII FMC].

Bottom line: state insurance lien-reduction statutes can limit an insured plan’s recovery, but cannot limit a self-funded plan’s clear contractual reimbursement rights. That federal-state balance is central to evaluating ERISA liens in Texas, California, and Illinois.

Which U.S. Supreme Court cases control ERISA reimbursement rights?

Several Supreme Court decisions define the contours of ERISA reimbursement and subrogation:

- Great-West Life & Annuity Ins. Co. v. Knudson, 534 U.S. 204. ERISA § 502(a)(3) authorizes only equitable relief, not legal damages against general assets. A plan must target specific funds or property in the defendant’s possession [LII Knudson].

- Sereboff v. Mid Atlantic Medical Services, Inc., 547 U.S. 356. A plan can enforce an equitable lien by agreement against specifically identifiable settlement funds in the participant’s possession, if the plan terms create a right to that fund [LII Sereboff].

- U.S. Airways, Inc. v. McCutchen, 569 U.S. 88. Clear plan language governs. Equitable doctrines like make-whole and common fund cannot override unambiguous plan terms requiring full reimbursement. If the plan is silent on fees, common fund may fill the gap [LII McCutchen].

- Montanile v. Board of Trustees, 577 U.S. 136. If the participant dissipates the specifically identifiable settlement funds on nontraceable items, the plan may not recover from the participant’s general assets under § 502(a)(3) [LII Montanile].

- FMC Corp. v. Holliday, 498 U.S. 52. State anti-subrogation laws are preempted as applied to self-funded ERISA plans, but may apply to insured plans via the savings clause [LII FMC].

These cases are repeatedly cited by federal courts in Texas, California, and Illinois when resolving ERISA lien disputes.

Do the make-whole and common fund doctrines reduce ERISA liens?

It depends on the plan language. In McCutchen, the Court held that unambiguous plan terms control. If the plan explicitly disclaims the make-whole doctrine and states first-priority reimbursement regardless of whether the participant is fully compensated, courts will apply those terms [LII McCutchen].

However, if the plan is silent about attorney’s fees, the common fund doctrine may apply to require the plan to bear its fair share of the fees necessary to create the settlement fund. McCutchen recognized that courts can use background equitable principles to fill gaps where the plan does not speak to a specific issue [LII McCutchen].

State law versions of these doctrines may still protect participants in insured plans under the savings clause, as explained below for Texas, California, and Illinois, while self-funded plans usually rely on federal preemption and clear plan terms to avoid reductions.

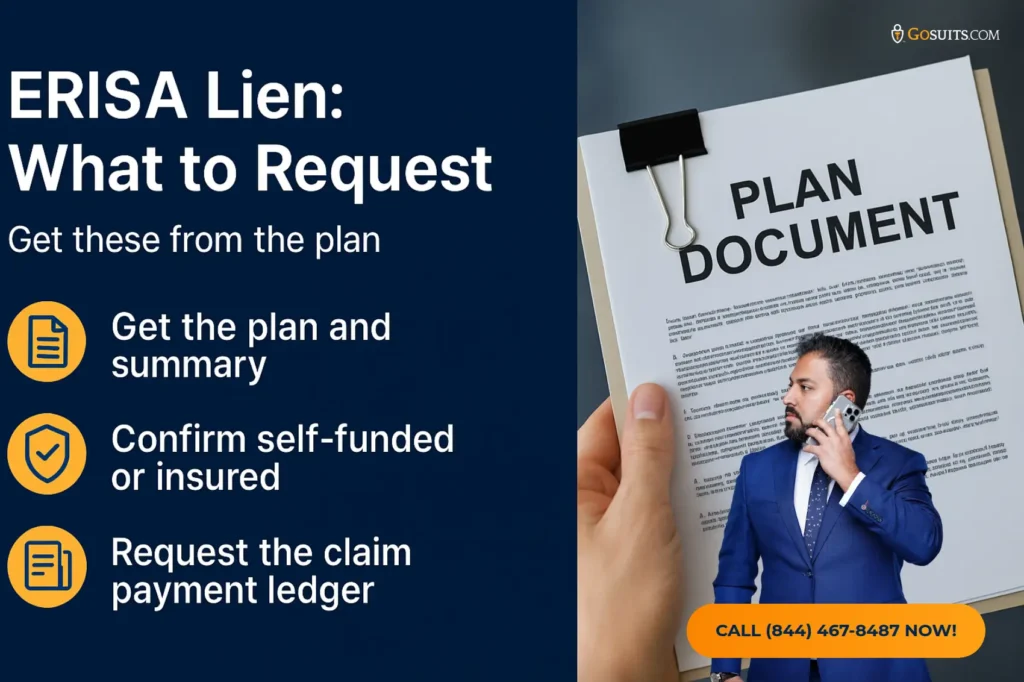

What documents should you request from the plan administrator to audit an ERISA lien?

Requesting the right documents early can change the outcome. Under ERISA, participants and beneficiaries can request plan documents, including the summary plan description and relevant instruments under which the plan is established or operated. See 29 U.S.C. § 1024(b)(4) [LII §1024], and SPD content requirements at 29 U.S.C. § 1022 and 29 C.F.R. § 2520.102-3 [LII §1022] and [eCFR 2520.102-3]. Failure to timely furnish documents may expose the administrator to statutory penalties under 29 U.S.C. § 1132(c)(1) [LII §1132].

Ask for:

- Complete plan document and SPD, including all amendments in effect on the date of injury.

- Subrogation and reimbursement provisions, including definitions of third party, first priority, and allocation of attorney’s fees and costs.

- Funding disclosures, showing whether the plan is self-funded or insured, and any stop-loss coverage details.

- Form 5500 filings, or confirmation of any exemption from filing.

- Identification of the plan administrator and fiduciaries, and any recovery vendors authorized to act.

- Payment ledger of medical claims tied to the injury, with CPT/ICD codes, to remove unrelated charges.

How can you negotiate or reduce an ERISA health insurance lien?

Your options turn on the plan’s funding status and its wording:

- Audit the claimed charges. Verify that every dollar the plan seeks to recover was paid for accident-related treatment. Dispute duplicative or non-injury charges with documentation.

- Apply the plan’s own terms. If the plan is silent on fees, argue for a common fund reduction. If it is insured, evaluate controlling state law limits on reimbursement as described in the jurisdiction sections below.

- Leverage Montanile and Sereboff. Funds must be identifiable and within the control of the participant or counsel. Keep settlement proceeds in trust until the lien is resolved. Shielding funds allows measured negotiations while preserving defenses recognized by the Supreme Court [LII Montanile], [LII Sereboff].

- Use proportionality. Present a hardship and proportionality analysis where settlement value was limited by liability disputes, comparative fault, low policy limits, or severe offsets.

- Confirm funding status. If the plan is actually insured, state law may cap or reduce recovery. If it is self-funded, reductions are mainly achieved through plan-based arguments and equitable gap-filling if applicable.

- Coordinate with other liens. Medicare, Medicaid, TRICARE, or provider liens must be prioritized as required by law. Medicare has its own statutory framework under the Medicare Secondary Payer rules [CMS MSP].

Do not distribute funds until the ERISA lien is resolved or an agreement is obtained. Ask for written confirmation of any reduction or compromise from the plan administrator or authorized vendor.

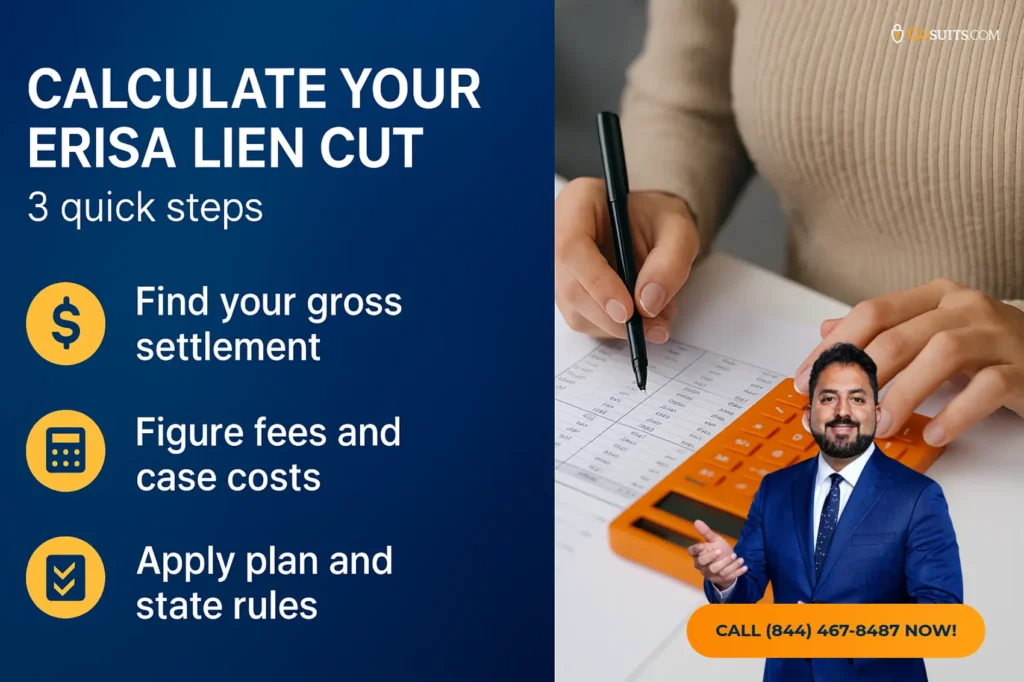

How do you calculate a potential ERISA lien reduction step by step?

Every case is different, but this sample framework illustrates common scenarios:

- Identify the gross settlement. Example: $100,000 from a car accident in Dallas.

- Determine attorney’s fees and costs. Example contingency fee of 33.33 percent and $3,000 in costs.

- Confirm plan language. If the plan is self-funded and explicitly disclaims make-whole and common fund reductions, courts frequently enforce first-priority rights under McCutchen.

- Common fund scenario if plan is silent. If silent on fees, allocate a proportionate fee to the lien. If the plan paid $30,000 in medical, a one-third attorney fee would reduce the lien by roughly $10,000, plus a proportion of costs, consistent with McCutchen’s gap-filling approach [LII McCutchen].

- State-law reduction for insured plans. If insured, apply state statutes like Texas Civil Practice and Remedies Code Chapter 140, which can cap the health insurer’s recovery under certain conditions [Texas CPRC ch. 140], or California Civil Code § 3040, which limits the amount a health insurer can be reimbursed from a third-party recovery [Cal. Civ. Code § 3040].

This illustration is not a guarantee of any outcome. The controlling plan text, funding status, and jurisdiction-specific law will drive the numbers. A personal injury lawyer can run this analysis with you to prevent avoidable overpayment.

How should defendants and insurers handle ERISA liens during settlement?

Defendants and liability insurers in Texas, California, and Illinois often face demands to protect ERISA liens. Practical steps include:

- Request lien information pre-settlement. Ask plaintiff’s counsel to confirm all known ERISA or health insurance liens and whether the plan is self-funded or insured.

- Avoid improper payees. Do not issue checks directly to an ERISA plan without the plaintiff’s consent unless required by court order or settlement agreement.

- Use lien holdbacks prudently. Where appropriate, a holdback in the plaintiff’s attorney trust account can protect all parties while preserving Sereboff and Montanile considerations about identifiable funds [LII Sereboff], [LII Montanile].

- Consider interpleader only when necessary. If competing claims threaten multiple liability, a court-supervised interpleader may be warranted. Federal courts have jurisdiction over ERISA disputes under 29 U.S.C. § 1132(e) [LII §1132].

How do ERISA liens interact with Texas law in Houston, Dallas, Austin, and San Antonio?

Texas has a detailed statute governing recovery by certain health benefit plans: Texas Civil Practice and Remedies Code Chapter 140. Among other things, Chapter 140 limits the recovery by a health benefit plan in third-party injury cases, applies formula caps, and addresses allocation of attorney’s fees and costs. These limits generally apply to insured plans, not to self-funded ERISA plans protected by ERISA’s deemer clause [Texas CPRC ch. 140], [LII §1144].

Texas case law historically allowed plan contract terms to override the make-whole doctrine for insured plans. The Texas Supreme Court decisions and the subsequent enactment of Chapter 140 shape today’s practice. Because self-funded plans derive their rights under federal law and often use explicit first-priority reimbursement language, they frequently resist reductions under Texas statutes. That is why confirming the plan’s funding status is critical for cases in Houston, Dallas, Austin, San Antonio, and across TX.

How do ERISA liens interact with California law in Los Angeles, San Diego, San Francisco, Sacramento, and Orange County?

California Civil Code § 3040 limits reimbursement by certain health insurers out of the injured person’s recovery. The statute provides a formula that may reduce the insurer’s lien based on the amount recovered and the insurer’s payments, and it accounts for attorney’s fees. Courts have applied § 3040 to health insurers and certain HMOs, but ERISA preemption shields self-funded plans from these limits. See § 3040 text and definitions [Cal. Civ. Code § 3040], and ERISA preemption at 29 U.S.C. § 1144 [LII §1144].

In practice, if your California case involves an insured plan, you may have arguments for a statutory reduction under § 3040 and for common fund allocation if the plan documents do not clearly negate fee apportionment. If the plan is self-funded, negotiations center on plan text and federal equitable principles recognized in McCutchen and Sereboff.

How do ERISA liens interact with Illinois law in Chicago, Springfield, and Naperville?

Illinois has long recognized the common fund doctrine in subrogation contexts, requiring a lienholder that benefits from a plaintiff’s attorney’s efforts to bear a proportionate share of the attorney’s fees. The Illinois Supreme Court’s decision in Scholtens v. Schneider, 173 Ill. 2d 375, applied the doctrine to an insurer’s subrogation recovery. While Scholtens addresses insured plans and state-law subrogation, a self-funded ERISA plan’s clear contract terms and federal preemption can limit the doctrine’s application. You can review Scholtens through public legal archives such as Google Scholar [Scholtens on Google Scholar].

Illinois also has lien statutes for healthcare providers, like the Health Care Services Lien Act, 770 ILCS 23, which regulates provider liens rather than health plan reimbursement. These provider liens often interplay with ERISA claims because they affect the distribution of limited settlement funds. The official Illinois statutes can be accessed through state resources and public legal libraries.

Do ERISA liens apply to wrongful death or loss of consortium claims?

Plan reimbursement rights typically attach to the participant’s recovery for injury-related medical expenses. Whether a plan can reach proceeds allocated to wrongful death beneficiaries or to a spouse’s loss of consortium depends on the plan text, the allocation in the settlement or judgment, and state substantive law defining those claims. Some plans define recoverable funds broadly, while courts may scrutinize allocations to determine what portion represents medical expenses paid by the plan. Clear, well-documented allocations and court approvals can help avoid after-the-fact disputes, subject to McCutchen’s rule that unambiguous plan language controls [LII McCutchen].

What happens if the settlement funds are spent before an ERISA plan seeks reimbursement?

Under Montanile, if the participant dissipates the specific settlement funds on nontraceable items, the plan may not recover from the participant’s general assets under § 502(a)(3). The plan’s equitable lien by agreement can only attach to specifically identifiable funds or traceable assets in the participant’s possession [LII Montanile]. That said, many courts consider the role of counsel as a constructive trustee when funds are held in trust, and plans often act promptly to prevent dissipation. Practically, parties and counsel should segregate settlement proceeds and avoid distribution until the lien is addressed.

How can GoSuits help you navigate ERISA liens with a technology-forward personal injury practice?

ERISA lien disputes can change your net recovery in a personal injury settlement. A free consultation with a personal injury lawyer can help you understand the plan documents, verify the plan’s funding status, and build a plan to address subrogation claims without delay. GoSuits represents injured people in Texas, California, and Illinois, including Houston, Dallas, Austin, San Antonio, Los Angeles, San Diego, San Francisco, Sacramento, Orange County, Chicago, Springfield, and Naperville.

GoSuits uses a technology-driven approach with exclusive proprietary software designed to gather plan documents, track deadlines, audit claim ledgers, and model various reduction scenarios quickly. This helps us surface negotiation leverage and reduce friction with plan administrators. While we use technology to move cases faster, every client works directly with a designated attorney. We do not assign case managers, and clients have direct access to their lawyer for strategy, updates, and settlement decision-making.

Our team brings 30 years of combined experience in serious injury cases. We prepare claims with trial in mind, which can strengthen bargaining positions with liability carriers and lienholders. Past results include seven-figure and high six-figure recoveries in motor vehicle and premises injury matters, with complex lien landscapes. You can see examples of prior cases here: GoSuits Prior Cases. Results depend on facts and law, and past outcomes do not predict future results.

Practice areas include car and truck collisions, wrongful death, dangerous property conditions, and other civil injury claims. We routinely coordinate ERISA subrogation, Medicare and Medicaid liens, and provider liens across TX, CA, and IL. During your free consultation, we can review plan documents, identify whether the plan is self-funded or insured, and outline the timeline to resolve the lien while protecting your settlement funds.

Where can you find official, trustworthy resources about ERISA liens and subrogation?

- ERISA civil enforcement, § 502(a)(3): 29 U.S.C. § 1132 LII

- ERISA preemption, savings and deemer clauses: 29 U.S.C. § 1144 LII

- Plan document and SPD rules: 29 U.S.C. §§ 1022, 1024; 29 C.F.R. § 2520.102-3 LII LII eCFR

- DOL ERISA overview: U.S. Department of Labor dol.gov

- Form 5500 information: DOL EBSA Form 5500 dol.gov

- Supreme Court decisions: Sereboff LII, McCutchen LII, Montanile LII, Knudson LII, FMC Corp. v. Holliday LII

- Texas insurance reimbursement limits: Tex. Civ. Prac. & Rem. Code ch. 140 capitol.texas.gov

- California insurer reimbursement limits: Cal. Civ. Code § 3040 leginfo.ca.gov

- Illinois common fund doctrine case: Scholtens v. Schneider, 173 Ill. 2d 375 Google Scholar

- U.S. Courts portal: Federal judiciary resources uscourts.gov

- Medicare Secondary Payer: Centers for Medicare & Medicaid Services cms.gov

- Health coverage statistics: U.S. Census Bureau, Health Insurance Coverage 2022 census.gov

- Injury burden context: CDC Injury Center overview cdc.gov

Frequently asked questions

Can a plan demand reimbursement greater than what it paid for accident-related care?

Plans generally seek to recover the amount they actually paid for injury-related medical claims. Auditing the ledger to remove non-injury items and write-offs can avoid inflated demands.

Can the plan recover from pain and suffering or wage loss portions of my settlement?

Many plans claim a right to reimbursement from any recovery, regardless of how it is labeled. Courts focus on plan language. If the plan asserts first-priority reimbursement out of any settlement, and is self-funded, courts often enforce that provision under McCutchen. If insured, state law limits may narrow the scope.

What if liability was disputed or there were low policy limits?

Present proportionality and hardship arguments. Even self-funded plans sometimes accept compromises where the recovery was constrained by liability or coverage barriers, especially if plan language allows discretionary reductions.

Does ERISA apply to government employees’ health plans?

Governmental plans and church plans are generally exempt from ERISA’s subchapter I under 29 U.S.C. § 1003(b). Different federal or state regimes may control those liens [LII §1003].

What official agencies oversee ERISA plans?

The U.S. Department of Labor, Employee Benefits Security Administration, provides ERISA compliance guidance for private-sector plans [DOL ERISA Overview]. Federal courts decide many ERISA disputes [U.S. Courts].

How often do ERISA liens affect car accident and serious injury cases?

Given that a majority of people have employment-based coverage nationally, ERISA liens are common in car accident cases in Los Angeles, Houston, Chicago, San Diego, Austin, San Antonio, San Francisco, Sacramento, Orange County, Springfield, and Naperville. Settlement values are also often influenced by injury severity. For context, national public health agencies track serious injury burdens and costs, which helps explain why healthcare payors pursue reimbursement [CDC Injury Overview].