- What is insurance stacking in California and why does it matter after an LA car crash?

- Is stacking UM/UIM coverage legal in California?

- How does California Insurance Code section 11580.2 shape UM/UIM claims in Los Angeles?

- What is the difference between uninsured and underinsured motorist coverage in California?

- How do California’s anti-stacking rules apply to multiple vehicles on one policy?

- Can you stack multiple separate policies in California?

- How does setoff and the difference-in-limits formula work for UIM in California?

- How do Los Angeles car accident payouts change under the new 2025 minimum liability limits?

- How do you find every dollar of coverage after a serious LA crash?

- How do arbitration and deadlines work for UM/UIM disputes in California?

- How do other insurance, permissive use, employer vehicles, and rideshare policies interact with UM/UIM?

- What defenses do insurers raise in UM/UIM cases and how might plaintiffs respond?

- What if the insurer mishandles your claim or delays payment?

- How do liens, med-pay, and workers’ compensation affect your net recovery?

- How can a Los Angeles personal injury lawyer approach stacking and UM/UIM strategy?

- Can you see examples of California UM/UIM and anti-stacking calculations?

- About GoSuits and how we help Los Angeles crash victims

- Sources and references

What is insurance stacking in California and why does it matter after an LA car crash?

Insurance stacking means trying to combine limits from more than one auto policy or more than one vehicle’s coverage to increase the total available payout for a crash. After a serious Los Angeles collision, stacking questions often come up with uninsured motorist coverage and underinsured motorist coverage, commonly called UM and UIM. These cover you when the at-fault driver has no insurance or not enough insurance.

Los Angeles traffic risk makes UM/UIM a critical safety net. California reported 4,407 traffic deaths in 2022, an increase from prior years, according to the California Office of Traffic Safety, citing federal data OTS Traffic Safety Facts). In dense traffic corridors throughout Los Angeles County, severe injuries are common, and policy limits of at-fault drivers may be too low to cover medical care, lost income, and long-term needs.

Whether you can stack UM/UIM in California depends on several rules, including California Insurance Code section 11580.2 and the language in the policies involved.

Is stacking UM/UIM coverage legal in California?

California generally prohibits adding up multiple UM or UIM limits on the same policy for one crash. This is commonly called anti-stacking. However, if more than one policy applies to the same person for the same crash, there may be limited scenarios where another policy could apply after the primary policy is used, subject to the statute and the policies’ other insurance clauses.

Key takeaways about insurance stacking California rules:

- Intra-policy stacking is restricted by statute and typical policy language. You usually cannot add up UM/UIM limits from two different vehicles listed under the same policy for a single loss.

- Inter-policy coverage may be possible in specific situations where you are an insured under a separate policy, but it depends on priority rules, anti-stacking provisions, and other insurance clauses found in California Insurance Code section 11580.2 and the policies themselves.

- UIM is difference-in-limits in California, so even before anti-stacking comes into play, the formula reduces how much the UIM carrier owes based on the at-fault driver’s liability insurance.

How does California Insurance Code section 11580.2 shape UM/UIM claims in Los Angeles?

California Insurance Code section 11580.2 sets core rules for UM and UIM coverage. The statute requires insurers to offer UM/UIM with every auto policy unless the insured rejects it in writing, and it regulates how claims are made, how disputes are resolved, and how limits apply. You can read the current text on the state’s official code site Cal. Ins. Code § 11580.2).

Important statutory concepts:

- Mandatory offer: Insurers must offer UM/UIM with minimum limits unless rejected in writing.

- UIM difference-in-limits structure: UIM pays only to the extent your UIM limit exceeds the at-fault driver’s bodily injury liability limit.

- Exhaustion requirement: UIM benefits typically are not payable until the at-fault driver’s liability limits are exhausted by settlement or judgment.

- Arbitration: UM and UIM disputes about liability and damages are generally resolved by binding arbitration under section 11580.2, rather than a civil jury trial against your UM/UIM insurer.

- Anti-stacking framework: The statute limits adding UM/UIM limits across vehicles on the same policy and sets rules for handling multiple policies.

- Deadlines: The statute includes timing requirements for making a claim and demanding arbitration.

What is the difference between uninsured and underinsured motorist coverage in California?

UM covers you when the at-fault driver has no liability insurance or is a hit-and-run driver whose identity cannot be established. UIM applies when the at-fault driver has liability insurance but not enough to cover your damages, and your UIM limit is higher than the at-fault driver’s liability limit. The California Department of Insurance provides consumer guidance on UM/UIM and why it matters in our state California Department of Insurance UM/UIM guide).

In Los Angeles, UIM often becomes the focus in serious-injury cases. Because UIM is difference-in-limits, a policy with higher UIM limits can be critical if the at-fault driver carried only the minimum required by the California Vehicle Code.

How do California’s anti-stacking rules apply to multiple vehicles on one policy?

When one auto policy lists multiple vehicles, California’s anti-stacking rules generally prevent you from adding multiple UM/UIM limits together for a single injury claim. In practice, that means your recovery is capped at the single highest UM/UIM limit available under that policy for any one covered vehicle involved in the accident. This anti-stacking principle is part of California Insurance Code section 11580.2 and is commonly reflected in policy language.

Intra-policy anti-stacking typically works like this:

- One claim, one limit: Even if you paid separate UM/UIM premiums for several vehicles under one policy, you cannot multiply the available limit for a single crash.

- Highest applicable limit controls: If the policy has different limits for different vehicles, the highest limit applicable to the accident will govern.

- No double recovery: Payments from one coverage part generally reduce or eliminate any overlapping claim under another part of the same policy for the same damages.

Can you stack multiple separate policies in California?

Sometimes an injured person qualifies as an insured under more than one policy. Common examples include a personal auto policy plus a resident relative’s policy, or a policy covering a vehicle you occupied and a separate policy where you are a named insured. Whether you can access more than one policy depends on:

- California Insurance Code section 11580.2: The statute sets priority and anti-stacking rules for multiple policies.

- Other insurance clauses: Policies often contain coordination clauses that designate primary, excess, or pro rata sharing.

- Status of the insured: Your status as a named insured, family member, or permissive user matters.

- Exhaustion: UIM is typically excess and may require you to exhaust the at-fault driver’s policy first.

In limited scenarios, a second policy may apply once the first applicable UM/UIM policy is exhausted, but you still cannot add limits together in a way that defeats California’s anti-stacking regime. Each claim needs a careful reading of all applicable policies and the statute to confirm priorities and any remaining benefits.

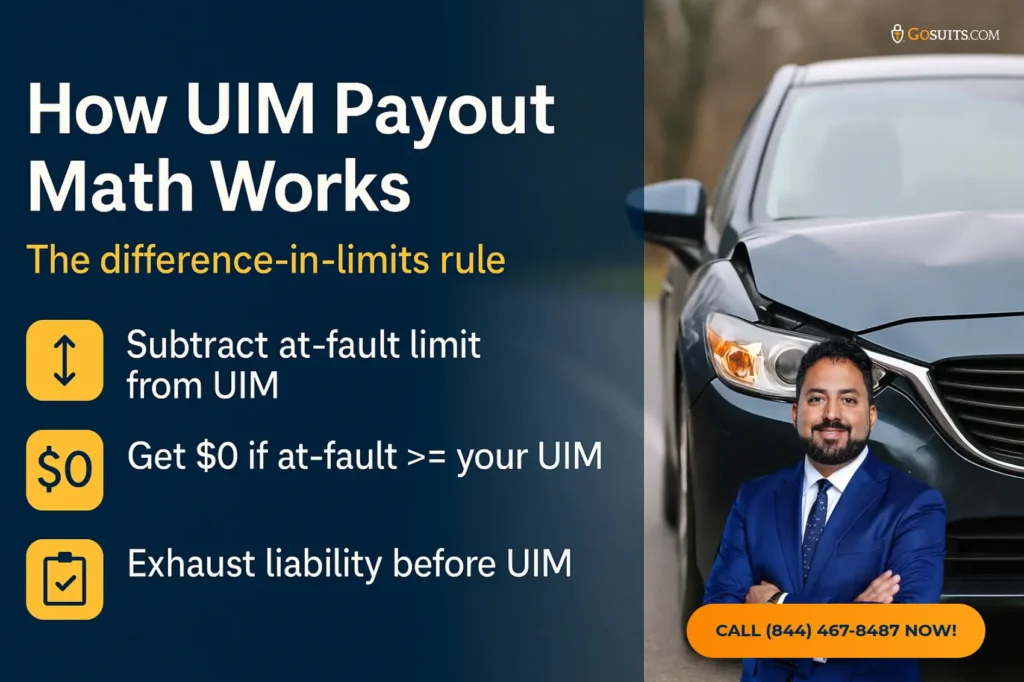

How does setoff and the difference-in-limits formula work for UIM in California?

California UIM is not add-on coverage for your total damages. It is difference-in-limits coverage. Under the statute, the UIM carrier’s maximum liability is your UIM limit reduced by the at-fault driver’s bodily injury liability limit paid to you. In short:

- If the at-fault limit equals or exceeds your UIM limit, your UIM carrier owes nothing because there is no difference to cover.

- If your UIM limit is higher than the at-fault limit, the maximum potential UIM payment is the difference between the two limits, up to your proven damages.

- Exhaustion applies. You generally must collect the full liability limit from the at-fault insurer before pursuing UIM, consistent with section 11580.2’s framework.

California Insurance Code section 11580.2 spells out this difference-in-limits structure and the effect of payments made by or on behalf of the underinsured motorist Cal. Ins. Code § 11580.2).

How do Los Angeles car accident payouts change under the new 2025 minimum liability limits?

Beginning January 1, 2025, California’s minimum auto liability limits increased to 30/60/15. This means:

- $30,000 for bodily injury or death to one person

- $60,000 for bodily injury or death to more than one person

- $15,000 for property damage

The California Vehicle Code requires proof of financial responsibility, and section 16056 sets these minimums. You can review the statute as amended and DMV guidance Cal. Veh. Code § 16056; see the DMV’s overview of financial responsibility requirements at DMV Financial Responsibility).

What this means for a Los Angeles car accident payout:

- Higher liability tenders from at-fault drivers who carry minimum limits.

- Different UIM math due to the difference-in-limits rule. If your UIM limit is 50/100 and the at-fault driver now carries 30/60, your potential UIM is the difference, subject to damages and stacking restrictions.

UM/UIM purchasing decisions matter more. Consider choosing UM/UIM limits well above the new minimums so UIM can meaningfully respond to serious injuries.

How do you find every dollar of coverage after a serious LA crash?

Locating all potential coverage is a key step in maximizing legal recovery within California’s anti-stacking framework. Consider these steps:

- Request all declarations pages for every household auto policy and any policy covering the vehicle you occupied, plus any applicable umbrella policy endorsements.

- Confirm UM/UIM selections and rejections in writing for each policy. The California Insurance Code requires specific procedures for rejecting UM/UIM offers.

- Identify permissive-use coverage on the vehicle you were in or driving, and whether you qualify as an insured resident relative elsewhere.

- Check employer coverage if you were on the job. Employer business auto policies can include UM/UIM with specific named insured definitions.

- Explore rideshare rules if Uber or Lyft was involved. These policies have tiered limits depending on the app status and may affect UM/UIM options.

- Verify med-pay and health coverage that can help with near-term bills and affect liens and offsets.

- Document injuries and losses to support arbitration on causation and damages, including medical records, wage documentation, and expert evaluations.

How do arbitration and deadlines work for UM/UIM disputes in California?

UM and UIM disputes typically go to binding arbitration under California Insurance Code section 11580.2. The statute also sets key timelines. One critical deadline is the time to commence arbitration or take qualifying action. The statute describes conditions and time limits for asserting these claims. Failing to timely demand arbitration can jeopardize your UM/UIM claim. See section 11580.2 for arbitration and limitations specifics Cal. Ins. Code § 11580.2).

Practical steps:

- Calendar demand deadlines immediately after the crash.

- Collect written consent from your UIM carrier before accepting the at-fault driver’s policy limits, so as not to impair subrogation rights.

- Prepare for arbitration early by building a record on liability and damages. Arbitration awards are limited to policy terms and limits.

How do other insurance, permissive use, employer vehicles, and rideshare policies interact with UM/UIM?

Coverage interactions in Los Angeles often involve more than one policy. Common intersections:

- Other insurance clauses: Policies may state that UM/UIM is excess over other collectible insurance or that the insurer will share pro rata. Section 11580.2 sets a framework and interacts with these clauses.

- Permissive use: If you were a permissive user of a friend’s car, their policy may be primary for liability and possibly UM/UIM. Your own policy could be excess depending on the language.

- Employer vehicles: Business auto policies can cover employees while driving for work. Whether UM/UIM applies depends on endorsements and named insured definitions. Workers’ compensation benefits may also be involved, which can affect offsets and lien rights under the statute.

- Rideshare tiers: If a rideshare app was on, coverage can vary by period. UM/UIM may be provided in certain periods. Check the rideshare company’s certificate and any period-specific endorsements.

What defenses do insurers raise in UM/UIM cases and how might plaintiffs respond?

In Los Angeles UM/UIM disputes, carriers frequently raise:

- Coverage defenses such as not an insured, not an uninsured or underinsured motorist event under the statute, or failure to exhaust the at-fault policy.

- Anti-stacking and other insurance to limit multiple policy recovery and designate priority.

- Late notice or missed arbitration deadlines under section 11580.2.

- Causation and damages disputes including preexisting conditions, comparative fault, and medical necessity.

Plaintiffs often respond by:

- Mapping status and policy definitions to show you qualify as an insured and that the crash falls within UM/UIM triggers.

- Complying with exhaustion and consent-to-settle provisions before invoking UIM arbitration.

- Proving damages with credible medical and economic evidence and addressing apportionment or comparative fault in arbitration.

What if the insurer mishandles your claim or delays payment?

California law imposes a covenant of good faith and fair dealing in insurance contracts. While UM/UIM disputes about the amount owed are commonly resolved through arbitration under section 11580.2, claim handling must still follow fair claims practices. If delays or denials are unreasonable, separate legal remedies may exist depending on facts and policy terms. Arbitration does not foreclose accountability for claim practices in all instances. Each situation is fact specific.

How do liens, med-pay, and workers’ compensation affect your net recovery?

Even when you recover policy limits, liens and offsets can change your net payout:

- Medical payments coverage can help pay bills early, but it may have reimbursement or coordination clauses.

- Health insurer liens and statutory reimbursement rights may apply and can sometimes be negotiated.

- Workers’ compensation can create liens and offsets. Section 11580.2 addresses credits in UM contexts to avoid double recovery, and policy language may contain additional coordination terms.

Because UIM is difference-in-limits, many offsets happen before UIM is even calculated. Careful coordination can prevent accidental waivers and protect your net recovery.

How can a Los Angeles personal injury lawyer approach stacking and UM/UIM strategy?

UM/UIM in California hinges on statute and policy language. A lawyer’s role includes:

- Policy audit: Gathering every potentially applicable policy and endorsement, identifying status as insured, and mapping other insurance clauses against section 11580.2.

- Timeline control: Preserving the UM/UIM claim by satisfying notice, consent-to-settle, and arbitration demand deadlines under the statute.

- Liability and damages proof: Building a persuasive arbitration file with testimony, records, and expert opinions, particularly where comparative fault or causation is disputed.

- Negotiation and sequencing: Exhausting the at-fault liability limits at the right time, then pursuing UIM with a complete damages package to support full difference-in-limits recovery.

- Lien management: Minimizing liens to protect the client’s net recovery, within legal and contractual constraints.

Self-representation against insurers is challenging, especially where anti-stacking California rules, difference-in-limits setoffs, and arbitration procedures intersect. Legal help can be important to navigate the statute and maximize available coverage.

How does a basic UIM difference-in-limits calculation work in Los Angeles?

Example A: You carry UIM limits of $100,000 per person. The at-fault driver carries the 2025 California minimum of $30,000. You settle with the liability insurer for the full $30,000. Your potential UIM is $100,000 minus $30,000, or up to $70,000, if your proven damages exceed $30,000 and within policy terms.

Example B: You carry UIM limits of $50,000 per person. The at-fault driver has $50,000 liability. Because the at-fault limit equals your UIM limit, there is no UIM payout, even if your damages exceed $50,000.

What happens if my own policy lists multiple vehicles with UM/UIM?

Example C: Your single policy lists three cars, each with $100,000 UM/UIM. You were injured while riding in Car 1. Under California’s anti-stacking rules, you cannot add the three $100,000 limits. The most you can claim under that policy for one person’s bodily injury is $100,000, subject to the difference-in-limits rule for UIM.

Could a second policy help in some California cases?

Example D: You were a passenger in a friend’s car covered by Policy A that includes UM/UIM of $250,000. You also have your own Policy B with UM/UIM of $250,000. Depending on policy definitions and other insurance clauses, Policy A may be primary and Policy B may be excess. If Policy A exhausts and Policy B’s terms allow additional recovery, you may access Policy B up to its limit, subject to section 11580.2 and anti-stacking prohibitions. A full policy review is required to confirm.

How does the 2025 increase in minimum limits affect payouts?

Example E: Pre-2025 minimums were 15/30 for bodily injury. If your UIM was 100/300 and the at-fault driver had 15/30, your potential UIM was up to $85,000 per person. Post-2025, with at-fault at 30/60 and your same 100/300 UIM, the potential UIM per person is up to $70,000. The higher minimums help some crash victims because more liability money is available, but they slightly reduce the UIM difference where the at-fault is minimally insured.

About GoSuits and how we help Los Angeles crash victims

UM/UIM and anti-stacking issues often decide how much money is actually available after a serious LA collision. If your case involves uninsured or underinsured drivers, multiple policies, or questions about California Insurance Code section 11580.2, a free consultation with a personal injury lawyer can be helpful to sort out coverage, deadlines, and arbitration strategy.

GoSuits handles injury cases across Los Angeles, Southern California, and throughout California. Our team uses a technology-driven approach supported by exclusive proprietary software built to surface coverage faster, track medical evidence, and move cases with fewer bottlenecks. Although we leverage technology to expedite litigation and negotiation, every client has a designated attorney from start to finish. We do not route clients through case managers, and clients have direct access to their lawyer.

We have 30 years of combined experience and a history of results in complex injury matters. Our courtroom background means we prepare cases as if they will be tried, which can strengthen settlement posture and arbitration outcomes. You can review representative past results on our prior cases page GoSuits Prior Cases). Past results do not guarantee a similar outcome, but they show the kinds of disputes and coverages we have navigated for clients.

Practice areas include motor vehicle collisions, pedestrian and bicycle injuries, commercial vehicle and rideshare crashes, premises liability, and catastrophic injury. For UM/UIM claims, we focus on policy audits, anti-stacking analysis, arbitration readiness, and lien resolution so that recovery is not lost to procedural missteps.

Sources and references

- California Insurance Code section 11580.2, Uninsured and Underinsured Motorist Coverage. Official code text: California Insurance Code §11580.2 — Uninsured and Underinsured Motorist Coverage

- California Department of Insurance, Uninsured Motorist Coverage consumer guide: California Department of Insurance uninsured motorist coverage guide

- California Vehicle Code section 16056, financial responsibility minimum limits, as amended: Official text of California Vehicle Code section 16056

- California Department of Motor Vehicles, Financial Responsibility overview: California DMV financial responsibility overview

- California Office of Traffic Safety, Traffic Safety Facts and statewide data: California Office of Traffic Safety Traffic Safety Facts and statewide data