- What is a personal injury settlement negotiation and how does it usually start?

- What laws shape settlement talks and what can be used in court?

- How do attorneys value a case and calculate pain and suffering?

- What evidence and documentation persuade insurance adjusters?

- How is a demand letter in a personal injury case prepared and timed?

- How do negotiation rounds and counteroffers usually work?

- How do policy limits and coverage types shape negotiation strategy?

- How does comparative negligence affect the settlement number?

- How do liens and subrogation reduce or delay a payout?

- What is mediation in personal injury cases and when does it help?

- What is the average settlement timeline and what deadlines matter?

- What should you know about releases, confidentiality, and taxes on settlements?

- What mistakes should plaintiffs and defendants avoid during negotiations?

- How do California, Texas, and Illinois rules differ on key issues?

- Quick FAQs about UM or UIM, property damage, rental cars, and recorded statements

- About GoSuits

- References and Resources

What is a personal injury settlement negotiation and how does it usually start?

In most personal injury claims, the parties resolve disputes through voluntary settlement rather than a trial. A settlement is an agreement to exchange compensation for a release of legal claims related to an incident like a car accident, a truck crash involving an 18-wheeler or tractor-trailer, a motorcycle accident, a slip or fall in a store, a construction injury on a scaffold, or a defective product case. Settlement is a core part of the civil litigation process and is recognized in American law and procedure as a primary pathway to conclude cases efficiently [1].

Negotiations often begin once you complete initial medical treatment or reach maximum medical improvement. Your attorney investigates liability and damages, then sends a demand package to the at-fault party’s insurer. Negotiation might happen informally by phone or email, during structured mediation, or at a settlement conference ordered by the court. Throughout, both sides test each other’s risk tolerance, evaluate evidence quality, and measure potential trial outcomes against the certainty of a settlement today.

Insurers analyze your claim using internal guidelines and claims histories. Attorneys scrutinize facts, policy limits, comparative negligence issues, lien obligations, and the forum’s jury tendencies. Especially in significant injury matters like brain injury, tbi, concussion, or wrongful death claims, the process often includes retained physicians, life-care planners, and economists, whose opinions inform the range of settlement values.

Public safety statistics also frame negotiations. For example, national traffic fatalities remain high, with more than 42,000 deaths in 2022, a sobering backdrop that keeps liability and damages front of mind in auto, pedestrian accident, and big rig cases [15].

What laws shape settlement talks and what can be used in court?

Two legal pillars typically guide what gets said and what can be shown to a jury:

- Settlement communications inadmissible to prove liability: Under Federal Rule of Evidence 408, offers and statements made during settlement discussions are generally not admissible to prove or disprove the validity or amount of a claim. This encourages candid negotiation without fear those words will be used later at trial [2].

- State mediation confidentiality rules: States add layers of protection. For instance, California broadly protects mediation communications from disclosure in court [9], and Texas encourages alternative dispute resolution, including mediation, through its ADR statute [10].

These protections allow attorneys to explore settlement numbers, exchange analyses of damages, and propose creative solutions like structured settlements or high-low agreements. They also support more open discussion of weaknesses in a personal injury case without making admissions.

How do attorneys value a case and calculate pain and suffering?

Valuation blends facts, law, and practical risk analysis. Attorneys generally consider:

- Economic damages: Medical expenses, rehabilitation, future medical needs, lost wages, diminished earning capacity, property damage in a vehicle or commercial property damage claim, and out-of-pocket costs.

- Non-economic damages: Pain and suffering, loss of enjoyment of life, physical impairment, disfigurement, and mental anguish.

- Liability strength: Clear liability in a rear-end car accident may justify a higher settlement than a contested liability intersection collision or a slip case with weak notice evidence.

- Comparative negligence: Any shared fault may proportionally reduce recovery, as explained later.

- Insurance coverage: Policy limits and coverage types set ceilings and shape strategy.

- Venue and jury tendencies: Some jurisdictions historically award higher non-economic damages in severe injury matters such as brain injury or wrongful death.

Pain and suffering calculation: There is no universal formula. Attorneys may discuss a multiplier of economic damages or a per-diem approach, but the real driver is evidence that brings your experience to life. That includes treatment records, narratives from treating providers, functional limitations documented by therapists, and credible testimony from family and co-workers. In product liability or construction cases, lasting disability or need for assistive devices can substantially increase non-economic damages.

Future care and life-cycle costs: For clients with serious injuries, valuation may involve life-care planning, home modification costs, vocational impacts, and increased medical needs as you age. In a motorcycle accident with catastrophic spinal injury, for example, negotiation may center on whether the life-care plan cost projections are reasonable, necessary, and related to the crash, and whether the at-fault truck or big rig policy can meet those projected costs. Attorneys also assess Medicaid or Medicare implications, including potential future medical obligations connected to the settlement [13].

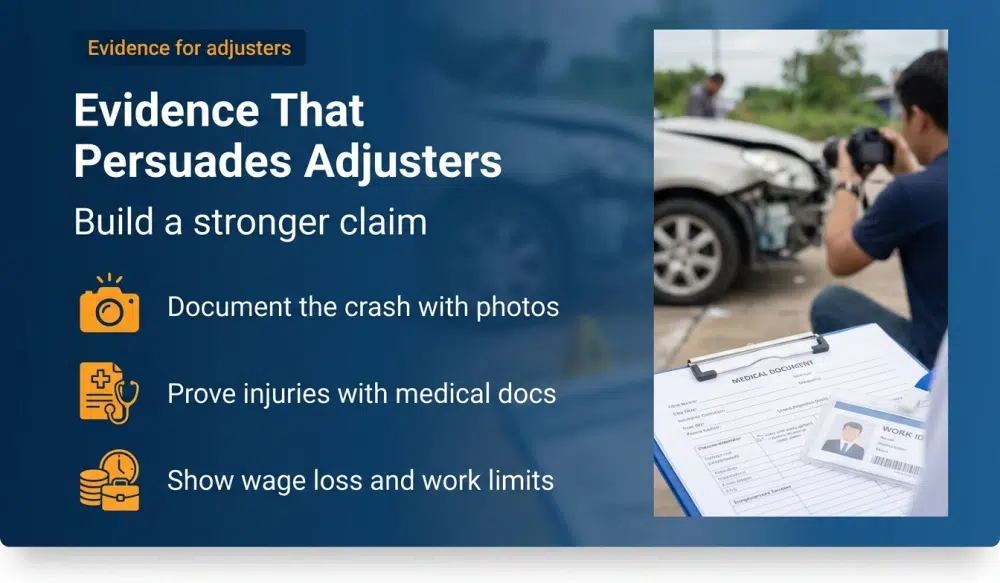

What evidence and documentation persuade insurance adjusters?

Negotiating with insurance adjusters is evidence driven. Strong demand packages usually include:

- Accident documentation: Police crash reports, incident reports for a trip or fall, OSHA records in a construction matter, and photographs or videos from dashcams, storefront cameras, or intersection devices.

- Witness statements: Neutral witnesses often carry significant weight. Where appropriate, a short declaration summarizing what they saw adds clarity.

- Injury proof: Emergency records, diagnostic imaging, operative reports, physical therapy notes, and treating physician opinions linking injuries to the incident.

- Functional loss: Work restrictions, job descriptions, employer letters, and disability documentation are powerful in lost wage claims.

- Property damage valuation: Repair bills, photographs, and appraisals support the force of impact in a car accident or the scope of harm in a commercial property damage claim.

- Insurance data: Policy declarations pages, proof of coverage limits, and any primary or excess policies relevant to a truck accident involving a semi or 18-wheeler.

Attorneys also manage pitfalls like gaps in treatment, preexisting conditions, or disputed causation in a brain injury, head injury, or concussion claim. Thorough and consistent medical documentation can neutralize these defenses.

How is a demand letter in a personal injury case prepared and timed?

A demand letter in a personal injury case, also called a demand package, frames liability, explains injuries, quantifies losses, and asks for a specific settlement within a deadline. It often includes:

- Liability synopsis: A clear, fact-based explanation of how the defendant is at fault.

- Injury overview: Diagnosis, treatment milestones, and prognosis in plain language.

- Damages summary: Medical bills, lost wages, and other economic losses with attachments.

- Pain and suffering narrative: How the injury changed daily living, hobbies, relationships, and work.

- Photographs and visuals: Before-and-after pictures, medical images, and diagrams.

- Settlement demand and deadline: A number supported by evidence and an invitation to discuss.

Timing matters. Sending a demand letter too early can cause undervaluation if treatment is incomplete. Sending it too late risks the statute of limitations, discussed below. In catastrophic cases like a tractor-trailer crash or wrongful death, attorneys may wait for key expert opinions before submitting a comprehensive demand.

How do negotiation rounds and counteroffers usually work?

Insurers rarely accept an opening demand. Instead, they reply with a reservation-of-rights letter and a counteroffer. Attorneys respond with additional records, clarifications, or updated bills. The process continues until both sides reach a number or decide to mediate or litigate.

Common settlement negotiation tactics include:

- Anchoring high or low: Plaintiffs may open with a higher number to anchor the range. Insurers may open low to test resolve.

- Bracketing: Proposing a range to see whether the parties can agree on a target zone.

- Incremental concessions: Small moves signal a near-bottom or near-top number.

- Conditional offers: Agreeing on total if specific liens are reduced or if a release contains certain terms.

- Time-limited demands: Encouraging timely valuation, especially when policy limits are implicated.

While offers made during negotiation usually are not admissible to prove liability or amount because of evidence rules like FRE 408 [2], attorneys still craft communications carefully. The goal is to educate the adjuster, build credibility, and demonstrate readiness for trial if negotiation fails.

How do policy limits and coverage types shape negotiation strategy?

Coverage fundamentally influences settlement strategy in personal injury settlement negotiation:

- Bodily injury limits: These caps often control the practical ceiling. If a California car accident causes catastrophic injuries with medical bills exceeding the at-fault policy, counsel may prepare a policy-limits demand with a reasonable acceptance window to secure full limits.

- Excess and umbrella policies: In a Texas truck accident with a big rig, there may be excess or umbrella coverage. Attorneys formally request disclosure of all policies and explore additional responsible parties.

- Uninsured or underinsured motorist coverage: If the at-fault driver lacks adequate coverage, your own UM or UIM policy becomes crucial. Strategy changes because you now negotiate with your own insurer while preserving cooperation and proof obligations.

- Medical payments and PIP: These cover initial medical costs but may trigger reimbursement rights depending on state law.

- Policy exclusions and defenses: Coverage disputes can slow negotiations. Attorneys navigate exclusions, reservations of rights, and potential declaratory judgment actions.

Insurer claim-handling standards exist in every state. For example, California has Fair Claims Settlement Practices Regulations that set timelines and conduct standards for claim evaluation and payment [12]. Knowing these frameworks helps counsel push for timely and fair review.

How does comparative negligence affect the settlement number?

Comparative negligence reduces recovery in proportion to the plaintiff’s share of fault. The rules vary by state, so nationwide cases must be analyzed by forum:

- California: Pure comparative negligence under Li v. Yellow Cab allows recovery even if a plaintiff is mostly at fault, reduced by their percentage of fault [8].

- Texas: Modified comparative negligence bars recovery if the plaintiff is more than 50 percent at fault, and otherwise reduces damages by their percentage [6].

- Illinois: Modified comparative negligence bars recovery above 50 percent fault and reduces damages below that threshold [7].

Practically, if an Illinois motorcycle accident claim has $200,000 in damages and the plaintiff is 25 percent at fault, the maximum settlement value is around $150,000 using the statute’s framework [7]. Comparative negligence disputes are frequent in intersection collisions, lane-change cases, or trip hazards in a slip and fall accident.

How do liens and subrogation reduce or delay a payout?

Liens and subrogation protect payers who covered your bills. They must often be resolved before disbursement:

- Medicare: The Medicare Secondary Payer statute requires reimbursement from settlements where a third party is responsible [13]. The Centers for Medicare and Medicaid Services administers conditional payments and recovery, which can delay or reduce net recovery if not addressed early [11].

- Medicaid: State Medicaid programs assert liens that must be resolved pursuant to federal and state rules. Early notice and documentation help reduce disputes about relatedness and amounts.

- Private health insurance and ERISA plans: Many plans assert reimbursement rights. Plan language determines scope and strength of recovery claims.

- Medical providers: Hospitals or clinics may record statutory or contractual liens where allowed.

Attorneys routinely negotiate lien reductions, especially where policy limits are low or injuries are significant. Defendants and insurers want lien clarity to avoid double payment risk, so organized lien resolution can accelerate the final settlement check.

What is mediation in personal injury cases and when does it help?

Mediation in personal injury cases is a confidential meeting with a neutral mediator who facilitates negotiation. It is voluntary in many courts, though some judges strongly encourage it. Mediation can resolve disputes that stalled due to credibility differences, valuation gaps, or lien disagreements. Communications in mediation are generally protected by state laws like California’s mediation confidentiality and by court rules favoring candid settlement discussions [9] [10].

Good mediation preparation includes updating medical specials, clarifying subrogation and liens, preparing a concise mediation brief, and planning minimum and stretch goals. In a wrongful death case or a severe tbi matter, mediation may be the first setting where carriers and defense counsel see the human story in full, which can move numbers significantly.

What is the average settlement timeline and what deadlines matter?

There is no single average settlement timeline because injuries, treatment length, coverage disputes, and litigation pace vary. Still, a common sequence looks like this:

- First 1 to 3 months: Investigation, liability assessment, early medical treatment, property damage handling, rental car issues, and initial communications with insurers.

- 3 to 9 months: Continuing treatment, collection of records, lost wage documentation, and draft of the demand letter personal injury package.

- 9 to 12 months: Negotiation rounds, counteroffers and demand packages, decision about mediation or filing suit if numbers stay far apart.

- Litigation path: If suit is filed, calendars depend on local court congestion, discovery needs, expert disclosures, and dispositive motions. Negotiation continues throughout.

The most critical deadline is the statute of limitations. Examples include two years for most California personal injury claims [3], two years for many Texas personal injury claims [4], and two years in Illinois for actions for damages for an injury to the person [5]. Shorter or longer periods may apply for claims against public entities, minors, or specialized statutes. Filing suit before the deadline preserves your rights and maintains negotiation leverage.

What should you know about releases, confidentiality, and taxes on settlements?

Settlement agreements include a release of claims and often other terms:

- Scope of release: Identify parties released and claims covered, including unknown or future claims where permitted by state law.

- Confidentiality: Many defendants request confidentiality to resolve high-profile matters like a construction fatal incident or product liability claim. Plaintiffs should weigh the pros and cons of secrecy and any liquidated damages terms.

- No admission of liability: Defendants typically include language denying fault.

- Tax considerations: As a general rule, amounts received for physical injuries or physical sickness that you did not itemize for medical deductions are excluded from gross income, while interest and some non-physical damages may be taxable. The IRS provides guidance that helps people understand typical treatment of different components of settlements [14].

Attorneys tailor releases to address structured settlements, indemnification for liens, Medicare reporting, and special needs trusts where appropriate.

What mistakes should plaintiffs and defendants avoid during negotiations?

- For plaintiffs: Avoid gaps in treatment without good reason, posting on social media about activities inconsistent with claimed limitations, ignoring lien notices, or missing statute deadlines. In a car or motorcycle claim, do not provide recorded statements to the adverse insurer without your attorney present.

- For defendants and insurers: Avoid undervaluing clear liability cases, disregarding evidence of future medical needs in a brain injury or concussion case, or ignoring claim-handling standards that could be scrutinized later under state insurance regulations [12].

- For both sides: Avoid personal attacks. Keep the focus on evidence, risk, and practical solutions.

How do California, Texas, and Illinois rules differ on key issues?

- California: Two years for most personal injury claims [3].

- Texas: Two years for many personal injury claims [4].

- Illinois: Two years for actions for damages for injury to the person [5].

Special rules apply for minors, government entities, and certain claim types. Filing early protects your rights and improves access to evidence and witnesses.

How does comparative negligence differ among these states?

- California: Pure comparative negligence permits recovery even when the plaintiff is mostly at fault, reduced by their percentage [8].

- Texas: Modified comparative negligence bars recovery over 50 percent fault and reduces by the share of responsibility below that threshold [6].

- Illinois: Modified comparative negligence with a 51 percent bar rule [7].

What about mediation confidentiality or ADR support?

- California: Strong mediation confidentiality statutes limit admissibility of mediation communications [9].

- Texas: The ADR statute promotes mediation and other alternative resolution processes [10].

How do unfair claim practices laws influence negotiations?

Claim-handling standards require timely, fair evaluations and communications. California’s Fair Claims Settlement Practices Regulations provide detailed timelines and duties that influence negotiation pace and content [12]. Other states have comparable frameworks in their insurance codes or regulations.

What practical steps can strengthen your settlement position starting today?

- Seek prompt care and follow treatment plans: Consistent medical records are essential for causation and damages.

- Preserve evidence early: Save photographs, witness information, 911 records, and videos from the scene of a crash, a worksite construction incident, or a defective product harm.

- Document wage loss: Collect pay stubs, tax forms, and employer letters.

- Track out-of-pocket costs: Keep receipts for medications, medical equipment, transportation, and home assistance.

- Be careful with social media: Avoid posts that contradict your claimed limitations after a collision or a fall.

- Consult counsel early: Early strategy affects liability investigation, medical proof, negotiation with insurance adjusters, and the statute of limitations and settlements timing.

How GoSuits Personal Injury Lawyers Can Help You

If you are navigating a personal injury settlement negotiation after a car accident, a motorcycle crash, a truck collision with an 18-wheeler, a slip or fall, a worksite construction incident, a brain injury, a wrongful death, or a product liability claim, a free consultation can help you understand options, timelines, and the documentation needed to support your case. We handle cases nationwide. Our firm leverages exclusive proprietary software to build demand packages faster, surface key evidence, and model ranges based on policy limits and comparative negligence. Technology moves your case forward quickly, and every client has a designated attorney with direct access at all times. We do not use case managers.

Our team brings 30 years of combined experience and real trial backgrounds that translate into stronger negotiating positions. We have recovered significant results for clients in diverse injury cases while maintaining a personalized approach informed by data. Explore representative outcomes at prior cases, learn about the trial lawyers who would handle your case at our attorneys, and see how we operate at about us. For a full list of what we handle, visit practice areas. We are ready to help you plan next steps, protect deadlines, and coordinate the medical, lien, and coverage issues that shape settlement value.

References and Resources

- Settlement – Legal Information Institute, Cornell Law School

- Federal Rule of Evidence 408 – Legal Information Institute, Cornell Law School

- Cal. Code Civ. Proc. § 335.1 – California Legislative Information

- Tex. Civ. Prac. & Rem. Code § 16.003 – Texas Statutes

- 735 ILCS 5/13-202 – Illinois Compiled Statutes

- Tex. Civ. Prac. & Rem. Code Chapter 33 – Proportionate Responsibility

- 735 ILCS 5/2-1116 – Illinois Compiled Statutes

- Li v. Yellow Cab Co. of California, 13 Cal.3d 804 – CourtListener

- Cal. Evid. Code § 1119 – California Legislative Information

- Tex. Civ. Prac. & Rem. Code Chapter 154 – Alternative Dispute Resolution

- Medicare Secondary Payer Overview – Centers for Medicare & Medicaid Services

- Fair Claims Settlement Practices Regulations – California Department of Insurance

- 42 U.S.C. § 1395y – Medicare as Secondary Payer – Legal Information Institute

- Publication 4345, Settlements Taxability – Internal Revenue Service

- Traffic Fatalities 2022 Final Data – National Highway Traffic Safety Administration